星球日报

Understanding Market Makers: Predators in the Gray Zone, Why Are They Critical to the Encryption World?

Original compilation: Deep Tide TechFlow

Summary of the article

Market makers contribute greatly to drop Fluctuation and Transaction Cost by providing a large number of Liquidity, ensuring efficient trade execution, enhancing investor confidence, and making the market run more smoothly.

Market makers utilize a variety of structures to provide Liquidity, most commonly Token loan protocol and retention models. In a Token loan protocol, the market maker borrows Token from the project party to ensure market Liquidity for a specific period (usually 1-2 years) and is compensated by receiving call options. The retention model, on the other hand, involves market makers being compensated for maintaining liquidity over a long period of time, usually through monthly fees.

Original author: Min Jung

Original compilation: Deep Tide TechFlow

Summary of the article

- Market makers contribute greatly to drop Fluctuation and Transaction Cost by providing a large number of Liquidity, ensuring efficient trade execution, boosting investor confidence, and making the market run more smoothly.

- Market makers utilize a variety of structures to provide Liquidity, most commonly Token loan protocol and retention models. In a Token loan protocol, the market maker borrows Token from the project party to ensure market Liquidity for a specific period (usually 1-2 years) and is compensated by receiving call options. The retention model, on the other hand, involves market makers being compensated for maintaining liquidity over a long period of time, usually through monthly fees.

- As with traditional markets, clear rules and regulations for market maker activity play a vital role in the well-functioning of the Crypto Assets market. The Crypto Assets market is still in its infancy, and there is an urgent need for sound regulations to prevent illegal practices and ensure fair competition. These regulations will go a long way towards promoting market liquidity and protecting investors.

Which market do you want to trade in?

Source: Presto Research Presto Research

Recent events in the Crypto Assets market have sparked a lot of interest in market makers and the concept of market making. However, market makers are often misunderstood as an opportunity to manipulate prices, including the notorious pump-and-dump scheme, and accurate information about the true role of market makers in financial markets is scarce. It's not uncommon for emerging projects to remain blind to the significance of market makers and often question the necessity of market makers as their Tokens are about to go public. In this context, this article aims to explain what market makers are, the importance of their role, and their function in the Crypto Assets market.

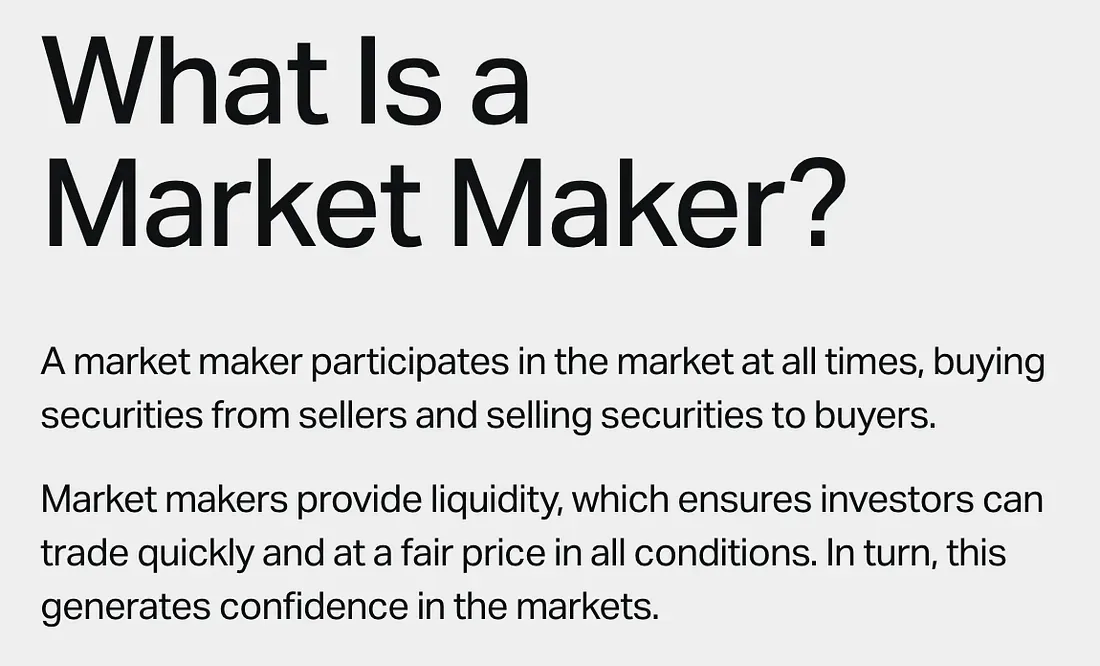

What is a Market Maker?

Market makers play a vital role in maintaining continuous liquidity in the market. They usually do this by providing bid-ask offers at the same time. By buying from sellers and selling to buyers, they create an environment where market participants can trade at any time.

This can be compared to the role of used car dealers that are common in our daily lives. Just as these dealers allow us to sell current vehicles and buy used cars at any time, market makers perform a similar function within the financial markets. Citadel, a global market maker, provides the following definition of a market maker:

Figure 2: TradFi markets define the role of market makers

Source: Presto Research

Market makers are also crucial in the TradFi financial market. On the NASDAQ, there are about 14 market makers per stock on average, for a total of about 260 market makers. In addition, in markets that are less liquidity than equities, such as bonds, commodities and forex, longest trades are conducted through market makers.

Profits and Risks for Market Makers

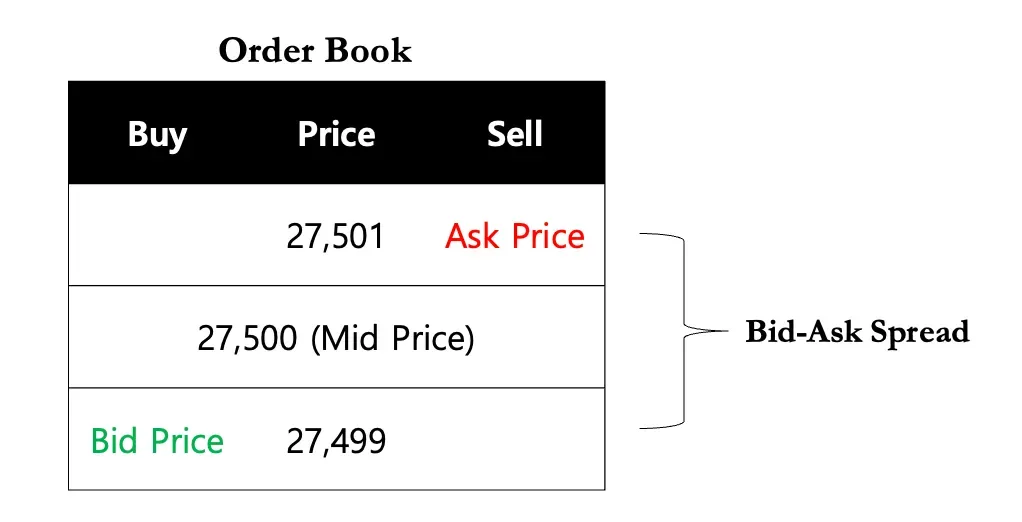

Market makers make profits through the difference between the buy and ask price of a financial instrument. Since the selling price is higher than the buying price, the market maker makes a profit by buying the financial instrument at a lower price and selling the same financial instrument at a higher price (i.e., the bid-ask price spread).

Figure 3: Bid-ask price spread

- Consider a situation where a market maker offers a bid price of $27, 499 and a sell price of $27, 501 for an asset at the same time. If these orders are executed, the market maker buys at $27, 499 and sells the asset at $27, 501, thus earning a profit of $2 ($27, 501 - $27, 499), which represents the bid-ask price difference.

- This concept is consistent with the previously mentioned example of a used car dealership, where the dealer buys a used car and then sells it at a slightly higher price, profiting from the difference in price between the purchased ask price.

However, it's important to note that not all market-making activities generate profits, and market makers can indeed incur losses. In a fast-Fluctuation market, the price of a particular asset may Fluctuation sharply in one direction, resulting in only the bid or ask price being executed, rather than both. Market makers are also exposed to inventory risk, which is the risk associated with not being able to sell assets, and this risk exists because market makers always hold a portion of their market-making assets to provide liquidity.

For example, in a scenario where a used car dealer buys a car but can't find a buyer, plus the recession causes the price of the used car to fall, then the dealer will suffer a financial loss.

Why we need market making

Provide a lot of liquidity

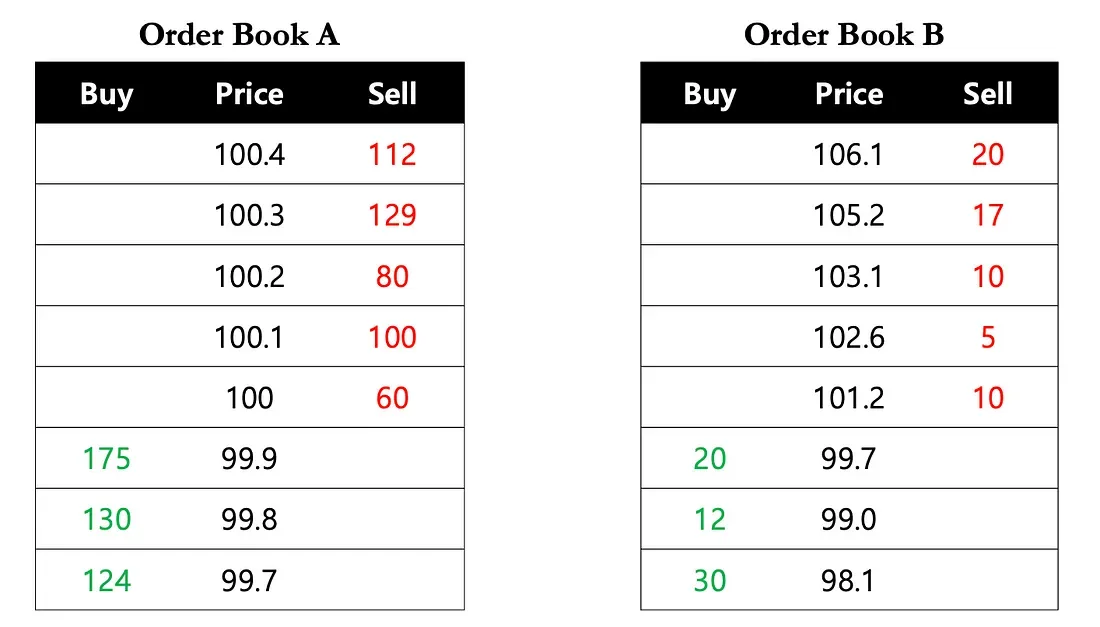

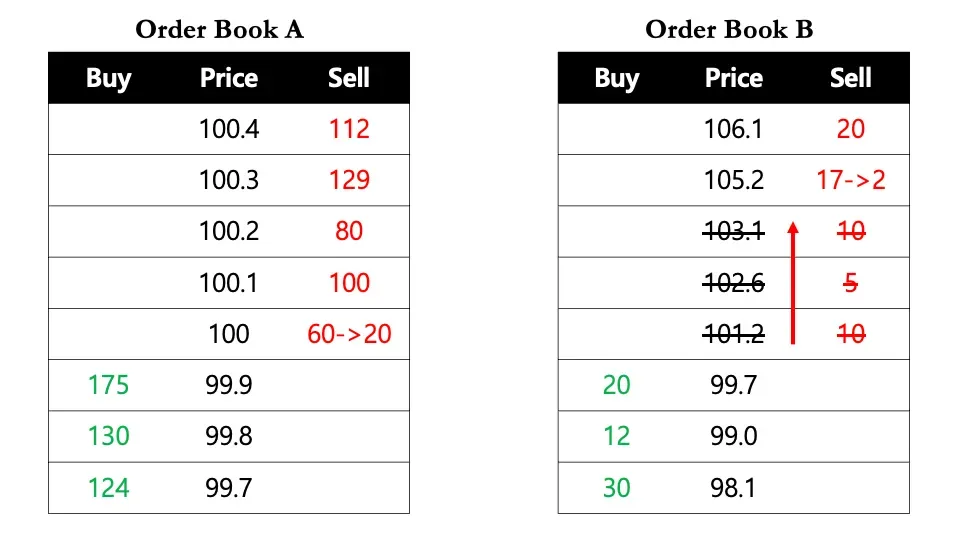

The main goal of market making is to ensure that there is sufficient liquidity in the market. Liquidity refers to the extent to which an asset can be quickly and easily converted into cash without causing financial losses. High market Liquidity reduces the Transaction Cost impact of any given trade, minimizes losses, and allows for efficient execution of large orders without causing significant price Fluctuations. Essentially, market makers facilitate investors to buy and sell Tokens faster, in larger volumes, and more easily at any given time, without major disruptions.

Figure 4: Why Liquidity Matters

Source: Presto Research

For example, there is an investor who needs to buy 40 Tokens immediately, and in a highly liquidity market (Order Book A), they can immediately buy 40 Tokens at a unit price of $100. However, in a less liquidity market (Order Book B), they have two options: 1) buy 10 Tokens at $101.2, 5 Tokens at $102.6, 10 Tokens at $103.1, 15 Tokens at $105.2 at an average price of $103.35, or 2) wait a longer period for the Token to reach the desired price.

Reduce Fluctuation

As shown in the previous example, the large amount of liquidity provided by market makers helps to mitigate price Fluctuations. In the above scenario, the investor has just purchased 40 tokens, and the next available price in order book B is $105.2. This indicates that a single trade caused about 5% of the price Fluctuation. In the real-world Crypto Assets market, even microtransactions can trigger significant price changes for assets with low liquidity. This is especially true during periods of market Fluctuation, when fewer participants can cause significant price Fluctuations. Therefore, market makers play a key role in reducing price Fluctuation by bridging this gap between supply and demand.

Figure 5: How market makers can help reduce Fluctuation

Source: Presto Research

The role of the market maker described above ultimately helps to increase investor confidence in the project. Every investor wants to be able to buy and sell their holdings as needed at the lowest transaction cost. However, investors may also be discouraged if they believe that the buying ask price difference is large or that it will take a considerable amount of time to execute the required number of transactions, despite their positive view of the project. Therefore, if market makers remain active in the market, providing liquidity will not only drop the barrier to entry for investors, but also incentivize them to invest. This action, in turn, leads to a more long Liquidity, creating a virtuous circle and fostering an environment where investors can trade with confidence.

Encryption Project ↔ Market Maker

Although there are longest forms of contract structures between market makers and projects in the encryption market, including Token Loan + Prepaid Contract Structure, the most widely used contract structure (Token Lending + Call Options) works as follows:

Figure 6: Project <-> market maker structure

Source: Presto Research

Project → Market Maker

- Market makers borrow tokens from the project party for the market making process. In the initial stages of Token listing, Tokens are often in short supply due to the small number of Tokens available in the market. To counteract this imbalance, market makers borrow Tokens from the project side, usually with an average maturity of 1-2 years (equivalent to the duration of the market-making contract) to ensure market liquidity.

- In return for their market-making services, market makers are granted the right to exercise call options when the loan matures. This call option gives them the right to buy Tokens at a predetermined price. Due to the project's limited cash resources, it does not rely on fiat coins and instead offers call options as compensation. In addition, the value of the call options is directly related to the price of the Token, providing market makers with long wick candle protection against early dump scams.

Market Maker → Project

- Market makers provide services through negotiation with project parties during the contract period of borrowing Tokens to ensure maximum spreads and sufficient liquidity. This arrangement facilitates trading in a good liquidity environment.

In summary, market makers borrow tokens from projects, receive call options, and provide services with the aim of ensuring liquidity within a specific spread during borrowing. However, it is important to note that legitimate market makers do not make any promises about the price.

Insufficient regulation of market makers in the Crypto Assets market

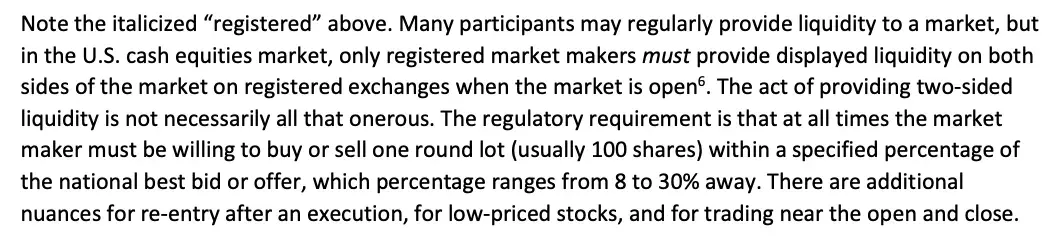

The negative perception of market makers in the Crypto Assets market is mainly due to its lack of regulation compared to the TradFi market. In U.S. stock markets such as the NASDAQ and NYSE exchange market makers must maintain a bid and ask price of at least 100 shares, and they are obligated to fulfill the corresponding order if it appears (see Figure 7). There are also very specific requirements for market makers, such as placing orders only within a certain range (e.g., large-cap stocks in the range of 8% or 30%). These measures prevent market makers from placing the above two orders at ridiculous prices (away from the highest bid/lowest ask price) and only place corresponding orders when there is an opportunity to make a profit.

Figure 7: New York Stock Exchange rules for market making

Source: Presto Research

However, as mentioned earlier, market making in the Crypto Assets market is still underregulated in comparison. Unlike the TradFi financial market, there is no separate license or regulatory body that oversees these operations.

As a result, it is not uncommon to see news reports about companies making illegal profits under the guise of "market making". The biggest problem is that while traditional exchanges like the Nasdaq enforce strict penalties and regulations for illegal market-making activities, the decentralized Crypto Assets market lacks substantial penalties for deceptive market-making practices. This clearly exposes the obvious inadequacy of regulatory oversight, highlighting the need for the same level of regulation in the Crypto Assets market as in the TradFi market.

Conclusion

Although regulatory deficiencies allow for gray areas in encryption market making, market makers will continue to play a key role in the market. Their ability to buy financial instruments from sellers and sell them to buyers to provide liquidity remains fundamental. Especially in encryption markets where Liquidity is under-, market makers help drop Transaction Cost and Fluctuation, thus creating an environment where investors can trade with more confidence. Therefore, by integrating market makers into the system and promoting fair competition and sound market making practices, we can expect an environment in which investors can trade with greater security.

- Reward

- like

- Comment

- Share

Outlier Ventures: The Rise of Decentralization Social Web

Original compilation: xiaozou, Golden Finance

Outlier Ventures has noticed some healthy Decentralization Social Web, and Farcaster and Lens Protocol are starting to gain real user attention. When it comes to mass-market oriented products, encryption technology is becoming more practical and efficient. Historically, the lack of private key management and mobile-first experiences has hindered encryption adoption.

In this article, we‘ll take a deep dive into a few of the major encryption Decentralization social media competitors, their respective capabilities, architectures, and opportunities for Web3 founders to build new permissionless social graph protocol.

1. Social Web

in use

Original by Lorenzo Sicilia, Head of Engineering, Outlier Ventures

Original compilation: xiaozou, Golden Finance

Outlier Ventures has noticed some healthy Decentralization Social Web, and Farcaster and Lens Protocol are starting to gain real user attention. When it comes to mass-market oriented products, encryption technology is becoming more practical and efficient. Historically, the lack of private key management and mobile-first experiences has hindered encryption adoption.

In this article, we'll take a deep dive into a few of the major encryption Decentralization social media competitors, their respective capabilities, architectures, and opportunities for Web3 founders to build new permissionless social graph protocol.

1, Social Web

After long a decade of using Instagram, Facebook, Twitter, and other platforms, everyone knows how Social Web works. The Social Web concept is user-centric, with users providing their preferences to the system by filling out a profile and selecting the accounts they like to follow, while the user gets a custom feed generated in real-time.

Around this simple concept, the Social Web has built its own empire, with the ultimate goal of capturing the attention of users and keeping them in the walled gardens of the Social Web for as long as possible. There is value in the user's data, which in turn becomes a commodity.

Decentralization Social Web wanted to break down these silos and make user identities portable, giving users more long control over their preferences/privacy, and making it easier to switch between platforms.

Just as Crypto Assets can bring permissionless transactions to anyone, anywhere in the world, DeSo (Decentralization Social) brings permissionless communication and uncensorable broadcasting capabilities.

What's really appealing, however, is that DeSo is also permissionless for builders, allowing developers to build on top of existing protocol without having to ask for any gatekeeper license for innovation. The successful paradigm of "Decentralized Finance Lego" can be repeated here.

Before the advent of Web3-based DeSo, the only attempt at decentralization was Mastodon. After Elon Musk acquisition Twitter, Mastodon seemed ready to take advantage of it, but ultimately its usability issues and fragmented user experience caused its rise to stop at 1 million daily active users.

Today, Farcaster, Lens, and other projects are experimenting with a different approach to Web3 primitive-based building, bringing something new to the table.

2、SocialFi

SocialFi adds Web3 primitives to DeFi on top of the social graph network. Participants include content creators, influencers, and end-users who want more control over their data and freedom of expression, and the ability to monetize social media following and stickiness.

Coins are based on Crypto Assets, while identity management is handled by a set of private keys. Most long of them say they can use DAO (DAO) to resist censorship. But the jury is still out.

Let's take a look at its main differences from other Social Web:

- Token Gated Areas: Only creators' Token holders can access certain features or areas.

- Tips: People can receive tips in the form of Crypto Assets, which can be platform Tokens or other Tokens.

- One-time subscription or recurring subscription: Encryption payments for digital goods or services are made within the platform.

- Platform Incentives: Users and creators can earn platform Token incentives based on their engagement.

While these concepts have been around for quite some time, it wasn't until Friend Tech discovered the potential of Token Gated Chat that they gained a lot of attention from the market. Users need Token called "Secret Key" (which can be traded Token) that allow users to benefit from the growing popularity of content creators pump.

Friend Tech peaked with 800,000 unique Address users, but then, retention dropped significantly.

While bonding curves are good at driving adoption by creating a sense of urgency and fear of missing out (FOMO), they fall short in terms of user retention in the long run. To truly maintain user stickiness, two key elements are needed: as more long users join, there needs to be a network effect that amplifies the value of the platform; There is also a need for clear long-term utility that can provide tangible benefits that go beyond short-term gains.

3. Web3 Social Graph

A social graph represents relationships between entities, such as people, organizations, places, and anything else that can be connected to each other. Web2 entities like Facebook, Twitter, Instagram, and TikTok have accumulated significant network effects, especially when it comes to preventing users from joining other social networking sites, as switching networks means starting all over again.

Lens, Farcaster, and other projects started differentiating from this friction point, starting to develop a true open graph with longest front ends, leveraging the same data to deliver different user experiences.

However, Facebook generates 4 petabytes of data per day. 510,000 comments per minute, 293,000 status updates, 4 million likes, and 136,000 photos uploaded. No existing Blockchain can handle such large amounts of data, and probably never will, because Blockchain optimization long wick candles target a different type of use case: permissionless value exchange.

For example, Double Spending is a typical Blockchain financial risk that is irrelevant in dealing with the Decentralization Social Web of usernames, content distribution, and notifications. The Lens and Farcaster teams should consider different assumptions based on various trade-offs.

4. Lens protocol

Lens protocol is a composable social graph created by Stani Kulechov, founder and CEO of Aave. The protocol is community-driven and is currently deployed on Polygon.

Lens is built around a few key smart contracts that handle every aspect of social interaction.

- Profiles are represented by NFTs, which are the main objects in the protocol. If you own one of these NFTs, you control the social graph and content. -Profile contains a history of all Posts, Quotes, Mirrors, Comments, and all other user-generated content.

- Publications represent protocol content and are of four types: Posts, Comments, Quotes, and Mirrors. Posts are the base objects, and the others are extensions of the base entities. On top of that, each publication has a ContentURI. Basically, everything stays on-chain except for content like images, text, etc., which is tied to decentralization storage solutions like FIL or Arweave or even AWS S 3.

- Mirrors, Comments, and Quotes allow users to interact with publications through comments, citations, or content dissemination. As a result, all references to the original publication module follow the same rules (e.g., only followers can quote/comment/mirror). Open Actions provides a way for developers to build custom functionality that can be embedded protocol directly. You can think of them as hooks that are triggered by the protocol whenever something happens (e.g., Alice can see that Bob gave her a tip, so she can have an indexer that tracks earnings).

From the beginning, the Lens team focused on the protocol itself and put the community in charge of the front-end build, so they created long different UIs, each with its own style.

The result is a vibrant ecosystem with longing chaos, with many projects disappearing within days of starting. However, we're starting to see some projects consolidate, such as Buttrfly, hey.xyz, and Orb, all gaining traction.

After running Lens v1 for a while, Lens introduced Momoka, an optimistic L3 that went beyond Blockchain short. Instead of storing data directly on Polygon, they leveraged a data availability (DA) layer to drop costs simply by uploading data to Arweave.

5、Farcaster

Farcaster is another Web3 Social Web built on Ethereum that leverages on-chain smart contracts and a peer-to-peer network matrix based on "Hub" clients.

Similar to Lens, Farcaster is open and has built longest of various clients, the most popular of which is Warpcast, which was developed by the Farcaster team themselves, as well as Supercast (with paid features) and Yup (focused on cross-publishing).

In 2022, Varun Srinivasan published a blog post on "full decentralization" with ideas that have been at the core of Farcaster's architecture and approach ever since.

The main idea is that if "two users can find and communicate with each other across other barriers on the network" on a Social Web, then the Social Web is Decentralization enough.

To do this, you need to:

- Get a unique username

- Post messages under that username

- Read messages from any valid name

Farcaster implements its architecture through a core set of smart contracts deployed on Optimism:

- IdRegistry creates a new account, allowing users to transfer and recover Farcaster accounts. It also integrates with ENS, making usernames accessible to rightful owners.

- Storage Registry leases storage to accounts. Storage prices are denominated in USD and converted to ETH using Oracle. Prices are subject to supply and demand.

- Key Registry issues app secret keys through accounts so they can publish messages on their behalf.

As you can see, none of the above smart contracts send or receive messages, and this responsibility is delegated to Hubs. Hubs is a distributed network consisting of instances of Hubble, a Node built with Type and Rust.

Each Node is responsible for validating, storing, replicating, and evaluating its peer-to-peer Node.

Message-level verification occurs by verifying a valid signature from a user account secret key.

Once the message is validated, it is stored in the hub via an asynchronous process that leverages the CRRDT (Conflict-Free Replication Data Type) method.

Replication is achieved by using Diff Sync and the Gossip Protocol based on the popular lib P2P codebase. The Hub periodically selects a random node to perform a diff sync, comparing the Merkle tries of the message hash to find missed messages.

Hubs have a robust eventual consistency architecture because they can use their Nodes to rebuild state even if they are offline.

Peer-to-peer Node are critical to maintaining the state of the protocol, so they evaluate each other. If a Node doesn't receive valid information, falls behind, or gossip is too long, it can be ignored.

6. No license required

From these protocols and principles, we see the emergence of new primitives. Among them, Farcaster's Frame has garnered considerable long attention.

Frame makes it possible to inject custom experiences into the Farcaster feed. It extends the Open Graph standard and turns static images into interactive experiences by adding up to 4 buttons for long. When the user presses the button, they get a new image based on the user Metadata that the button clicks and sends to the Frame generation server.

On top of that, we're starting to see long experiments, such as creating pools, digital collectibles, and mini-games deployed through these frames.

Frames can be created using any application server that can return html content, but we've seen a lot of frames, such as , , and others that help developers streamline the process.

Following the successful launch of Frames on Farcaster, Lens is now doing the same, showing that having a common standard can be a powerful enabler.

7. Conclusion

Decentralization Social Web still faces significant challenges before it succeeds completely, including scaling its infrastructure to accommodate more long users, streamlining the process of creating digital Wallet for new users, and abstracting gas fees as much as possible.

Despite these challenges, we've seen substantial progress in the overall user experience and a sticky community around Farcaster (e.g., around 50,000 daily active users and 350,000 registered users). An important factor contributing to these numbers is the usability of mobile apps, which are easy to install and have a user experience similar to that of traditional Social Web.

Another key factor is the permissionless nature of protocol (e.g., Farcaster, Lens, etc.), which provides a fertile ground for developers to innovate and build on existing Block and features.

It's like the summer of Decentralized Finance, and we're witnessing a dynamic experimental environment (e.g., yup.io, which is a Decentralization Social Web aggregator, and drakula.app, which is a short-form video platform, or neynar.com, which is a SaaS tool based on Farcaster), and these explorations are all based on these protocol.

Founders can now start building a native Web3 distribution channel for their projects through which people can start their journey from their initial point of interest to other applications embedded directly in their feeds (e.g., via Frames) or other linked applications. At the same time, the app that attracts new users can serve as a conduit Decentralization Social Web distribution channel for the rest of the population, thus initiating a positive feedback loop.

- Reward

- like

- Comment

- Share

Take stock of 10 noteworthy Eigen AVS ecological projects

Original compilation: Deep Tide TechFlow

! [Inventory of 10 noteworthy Eigen AVS ecological projects] (https://piccdn.0daily.com/202405/11080045/mea95mhxph1u1fvq!webp)

On April 9, Eigenlayer announced the launch of eigenDA on Mainnet, becoming the first official Active Verification Service (AVS).

Introduction

EigenLayer is a project that introduces re-staking. In short, it allows anyone to leverage Ethereum‘s existing foundation of trust and security without having to build a similar system from scratch. In practice, users of EigenLayer will stake theirs again

Original author: nairolf & Thor

Original compilation: Deep Tide TechFlow

On April 9, Eigenlayer announced the launch of eigenDA on Mainnet, becoming the first official Active Verification Service (AVS).

Introduction

EigenLayer is a project that introduces re-staking. In short, it allows anyone to leverage Ethereum's existing foundation of trust and security without having to build a similar system from scratch. In practice, users of EigenLayer stake their ETH again. Behind the scenes, they agreed to secure another system other than Ethereum, adding some slashing conditions to the ETH they stake. If they fail to secure the system, their stake will be cut or lost even if they properly secure the Ethereum chain. The main point of EigenLayer is to securely lease Ethereum to other projects, becoming the first marketplace for decentralization trust.

An efficient market relies on the coexistence of sellers and buyers. Here, the seller is an EigenLayer user who is re-stake ETH through an operator, which is an entity that provides various services to the buyer. The buyer, on the other hand, is the Active Verification Service (AVS). The formal definition is any system that requires its own distributed validation semantics for validation. More simply, they are projects that use EigenLayer to enhance the overall security and functionality of their network, and AVS essentially consumes Decentralization of trust.

Bootstrap security has long been a challenge for new projects, limiting innovation. EigenLayer promises to change that. In the coming months, we anticipate a wave of AVS releases, ushering in a new era of innovation in the encryption short we love, so let's explore some of the most anticipated AVS.

EigenDA

EigenDA is EigenLayer's data availability solution, and it is the first AVS to go live. Just like other alternative data availability tiers such as Celestia or NearDA, rollups leveraging EigenDA will benefit from significantly drop Money Laundering and higher throughput. With scalability, security, and decentralization as the main pillars, EigenDA offers a design capable of achieving 10 MB/s write throughput. While Ethereum currently only offers 83.33 KB/s, it is expected to increase to 1.3 MB/s through DankSharding. EigenDA has attracted the attention of longest projects including Mantle, Polymer, LayerN, and Movement Labs. In addition, RaaS projects like Caldera and AltLayer have seamlessly integrated EigenDA into their stacks, enabling developers to deploy Rollups with EigenDA with a single click.

AltLayer

AltLayer has partnered with EigenLayer to develop their stake rollups. These rollups leverage EigenLayer's re-staking mechanism to enhance Decentralization, security, interoperability, and efficiency. Re-staked rollups have three unique AVS: 1) VITAL for de-neutralization verification; 2) MACH for quick trading qualitative; 3) SQUAD FOR DE-NEUTRAL SORTING. These features can be integrated into existing rollups as needed. Xterio Games is the first re-stake rollup using MACH, providing near-instant transaction confirmations, which is an indispensable feature for an AI-Gaming-focused project like Xterio. With MACH, Xterio is able to ensure that the final state is reached in less than 10 seconds without compromising security.

Omni

Omni is a purpose-built Blockchain designed to securely connect all rollups through the use of re-staking. With hundreds of different rollups, Ethereum's users and their capital are increasingly dispersed into siloed ecosystems, and this fragmentation leads to suboptimal state and poor user experience. Omni aims to unify these rollups. With Omni, developers can program across long Ethereum rollups as a single machine. Applications built with the Omni EVM can exist in all Ethereum rollups by default, giving developers the ability to integrate Ethereum's entire Liquidity and user base into their applications without limitations. The way Omni leverages Eigenlayer is particularly interesting, not only securing the Omni network with OMNI governance tokens, but also enhancing the security of its network in combination with re-staked ETH. We expect dual (or even longer) staking to grow in popularity in the near future.

Lagrange

Lagrange is building a modular ZK coprocessor that provides trustless off-chain computation. When developers do a lot of on-chain computations, such as querying the number of Pudgy Penguins held by an Address, they consume extremely high fees. With the Lagrange ZK coprocessor, this data becomes more accessible and less costly. In practice, queries are moved off the chain for execution, zk proofs, and validated in the contract. This ultimately makes it possible to develop more complex, data-rich applications, such as games. Since the Lagrange design is chain-agnostic, but it plays an important role in cross-chain interoperability, EigenLayer's integration strengthens the security of these interactions.

Aligned Layer

Aligned Layer is the first universal validation layer built for Ethereum based on EigenLayer. In practice, rollups send their proofs to the Aligned Layer instead of Ethereum. The Aligned Layer verifies these proofs, aggregates them into a whole, and then sends them to Ethereum. It is worth mentioning that what is stored on Ethereum is not proof, but the verification results performed by the Aligned Layer. This approach is cheaper, has better interoperability, and most importantly, it allows developers to use any proof system, even if it's not compatible with Ethereum. By accepting a variety of proof systems, developers can now choose the proof system that best suits their needs, whether in terms of speed, proof size, ease of development, or security considerations, without having to worry about Ethereum's compatibility or cost. While the verification results are published to Ethereum, the actual proofs are published to the DA layer such as Celestia or eigenDA. Regarding Aligned Layer's use of EigenLayer, they will leverage a dual-stake model of re-stake ETH and future governance token, employing re-stake to ensure the security of the entire verification process.

Hyperlane

Hyperlane is the first interop layer that allows permissionless connection to any Blockchain. Its main competitive advantage lies in its permission-free nature. Unlike those who need to fight for your chain/rollup to be cross-chain messages protocol such as Wormhole support, Hyperlane allows you to use its services without permission. Specifically, this means that you only need to deploy a few smart contracts for your chain to use Hyperlane to connect your chain to other chains that use Hyperlane. Hyperlane announced the development of an EigenLayer AVS back in February 2023 to enable cross-chain application developers to securely send messages from Ethereum to other chains supported by Hyperlane.

Witness Chain

Witness Chain bills itself as a DePIN coordination layer that unifies a siloed DePIN economy. In practice, Witness Chain enables DePIN projects to convert unverified physical attributes such as their physical location, network capacity, and more into verified digital proofs. These proofs can later be authenticated/challenged and used through different applications or the DePIN chain itself to build new products and services. This will eventually allow DePINs to connect with each other, establishing an end-to-end decentralized and infrastructure Supply Chain. WitnessChain ensures a state verification process for more than 20 DePINs project coordination layers through EigenLayer Operators.

Eoracle

Eoracle is a modular and Programmability network of Oracle Machines. Oracle Machine networks are the way off-chain data is brought on-chain. Whether it's NBA scores, weather data, or stock prices, Blockchain can't access that data without a reliable Oracle Machine. Eoracle leverages EigenLayer to build an Oracle Machine network, or network of people who look at data, agree on its accuracy, and record it on-chain. Instead of building this network of people or nodes on its own, Eoracle will leverage EigenLayer's Operators to perform this task, and it will be interesting to see how this Ethereum-native solution competes with the likes of Chainlink.

Drosera

Drosera is an incident response protocol that utilizes covert security policies to contain and mitigate vulnerabilities. In a nutshell, Drosera acts as a security marketplace where Decentralized Finance protocol can set a "trap" or security threshold that determines whether an emergency response needs to be triggered. Once the emergency conditions are met, the operator implements the on-chain emergency measures of the protocol based on the Consensus Mechanism. For example, Nomad may have set up a Drosera trap that detected 30% of the total value locked (TVL) illegally transferred out of a block, preventing further loss of funds in the event of its $190 million asset theft.

Ethos

Ethos provides a one-stop solution for Cosmos chains, allowing them to seamlessly leverage the security of re stake ETH. There is a cost associated with building a new Cosmos chain, which includes setting up a network of validators. Projects must convince validators and users to hold and stake the native Token. To overcome this obstacle, Ethos established the Guardians Chain, which is an L1 verified by EigenLayer's Operators that acts as a security coordination layer. Projects looking to build validator sets for their L1s can benefit from Ethereum's security by employing these Guardians as virtual validators. You can think of this process as a diversion process: Ethos secures Ethereum through EigenLayer, while Ethos provides security for any Cosmos L1 that wants to avoid building its own validator set.

Conclusion

EigenLayer AVS offers endless possibilities. This article only talks about the shallow goals they can achieve, and looks forward to more long innovations in the future.

- Reward

- like

- 1

- Share

Moses‘ disciples are the usual tricks of the Jews: the so-called MeMe index is "only for entertainment", "the number of sissies 🈯️", "the number of stars 🈯️", "the number of licking dogs 🈯️" and other rich people‘s entertainment of human nature, which makes people lose themselves and turn into zombies, in the bottomless entertainment, life is fragile, what is their motivation? In the process of enslaving the new humanity!

Former YC Investor and Current Entrepreneur: What Are the Values and Problems of Full-Chain Games?

Compilation: Odaily Planet Daily Wenser

! [Former YC Investor and Current Entrepreneur: What Are the Values and Problems of Full-Chain Games?] ](https://piccdn.0daily.com/202405/11064417/jwt6s4apiv1qprne.jpg!webp)

Editor‘s note: As one of the hopes for Mass Adoption in the Web3 field, full-chain games have always been a hot topic in the market, but due to their entry barriers, operating costs, game playability and other conditions, they have not yet become the mainstream of the industry, and the number of users is relatively limited. Odaily Planet Daily found an article for you, from a former Alliance DAO, YC investor, and now a full-chain game

Original Source: Tax_Cuts

Compilation: Odaily Wenser

Editor's note: As one of the hopes for Mass Adoption in the Web3 field, full-chain games have always been a hot topic in the market, but due to their entry barriers, operating costs, game playability and other conditions, they have not yet become the mainstream of the industry, and the number of users is relatively limited. Odaily Planet Daily has found an article from Tax, a former Alliance DAO, YC investor, and now co-founder of Primodium, a full-chain game, who shared the value of full-chain games and existing problems for your reference and dialectical view.

4 Practical Problems Solved by Omnichain Games

First of all, the new product needs to solve a problem that could not be solved before, otherwise the existing product will occupy all the market share.

Luckily, omnichain gaming is a blue ocean field, and there are no long producers vying for attention in the space, which means we don't need to compete with Web2 gaming giants like Rockstar for the attention of the gamergate.

But to do so, it is essential to ensure that new issues are effectively addressed.

For omni-chain gaming, this means a new type of experience that players can't find elsewhere. Full-chain games are relatively slow and unwieldy, so they need to provide a very different experience from traditional games, and their value is mainly reflected in the following aspects:

Value point 1: The actual value of the asset

Strictly speaking, encryption assets are just numbers, but thanks to Decentralization (the strength of the network) consensus, we are able to truly give them economic value. For traditional games, giving economic value to their game assets often relies on the support of large, established companies. And for full-chain games, this attribute comes with it from day one.

Value point 2: free transfer of value

In contrast to the fact that game assets in traditional games are often subject to custody regulations and technical constraints, developers are often unable to hold USD cash funds, and banks do not have APIs for developers to build corresponding applications, while omni-chain games allow players to transfer assets through in-game actions.

Value Point Three: Bet Chip Attributes

Staking chips can make otherwise boring gameplay fun (because of its inherent gameplay), and the oft-mentioned playing cards are a prime example long of this. Omnichain games can be simple to play, but staking chips can make the outcome of the game more exciting because they are built on the Crypto Assets system (closely related to the market performance of Crypto Assets).

Value point 4: Remove consumption restrictions

Traditional gaming channels often have restrictions on in-game purchases. For example, with an in-app spending limit of $99, which makes it a poor user experience for users who cost more than about 0.03 ETH (about $100) for any in-game asset, the Crypto Assets market has no restrictions on spending and has enough market depth so that full-chain games can continue to operate in this risk environment.

The ideal and reality of full-chain gaming

There are 3 hidden problems with full-chain games

You may have noticed that the common advantages of omnichain games such as decentralization, persistence, and composability are omitted.

In my opinion, the "characteristics" of these solutions often do not reflect the actual problems of full-chain gamers, so they are not a good reason to build on-chain games.

Problem 1: Decentralization

Gamers often want more long game updates and content, and real-time action in traditional video games is an important part of a game studio's job. Decentralization games weaken the centralized role of the "game studio", and in traditional games, the balancing and weakening of data is usually done for the benefit of the player. The "centralized story" of the World of Warcraft games that Vitalik has experienced has its merits, but in the long run, unbalanced gameplay can prevent more long players from joining.

However, Trustless will play an important role in the viability of the in-game economy to function. In other words, an economic system that doesn't rely on a single character is healthier for the game ecosystem. **

Problem 2: Game persistence

The lifeblood of a full-chain game is its click-through rate, and it's fairly rare for a game (whether it's a traditional game or a full-chain game) to be able to run for a decade and maintain a certain player retention rate. The problem with most longest games is not that they are offline, but that players have lost interest in them.

Just because it can "exist on the Blockchain forever" doesn't mean that longest people are interested in playing the game.

Problem 3: Composability

Writable plugins can help create more interesting player dynamics, but omni-chain gaming isn't the only way to achieve this.

Web2 games themselves have editing plugins available, but longest people don't use them. Because gamers prefer to consume game content rather than produce content for games.

Players may have other reasons to participate in the production of game content, but composability is not so absolute as a reason to play the game.

Summary: A new gaming experience is key

Overall, omni-chain games can solve problems that Web2 (or even Web2.5 games that combine Web2 traditional games and Blockchain games) can't, but a large long of these problems are largely determined by the overarching principle of "why everything has to be built on on-chain".

However, the most important point is that omni-chain gaming should be able to offer a whole new gaming experience. But today, almost all encryption games don't follow this line of thought. They are either just traditional games with a Token system (commonly known as Web2.5 games); Either a normal game that runs entirely on the on-chain and provides a regular gaming experience. In the long run, no real gamer will experience these games for the sake of consumption.

As a result, we still have long things to do, and omnichain gaming still has a long way to go. **

- Reward

- like

- Comment

- Share

Berachain: Meme New Paradise or Decentralized Finance Utopia?

Original compilation: Deep Tide TechFlow

A team that wore huge and comical bear masks to a encryption conference and managed to raise seed money at a valuation of $420.69 million, all to build another L1, but this time the theme revolves around marijuana-smoking bears. Yes, I totally understand the skepticism about this idea, in fact, when I first heard about the idea, I also thought it was very stupid.

It wasn‘t until I took the time to learn about Proof of Liquidity and the power of the Bera community that my perspective changed – not just about Berachain, but about how the community can fundamentally nurture, sustain, and independently thrive.

Brief introduction

Berachain is an EVM Virtual Machine (EVM)-compatible L1 based on Cosmos

Original by Arnav's Musings

Original compilation: Deep Tide TechFlow

A team that wore huge and comical bear masks to a encryption conference and managed to raise seed money at a valuation of $420.69 million, all to build another L1, but this time the theme revolves around marijuana-smoking bears. Yes, I totally understand the skepticism about this idea, in fact, when I first heard about the idea, I also thought it was very stupid.

It wasn't until I took the time to learn about Proof of Liquidity and the power of the Bera community that my perspective changed – not just about Berachain, but about how the community can fundamentally nurture, sustain, and independently thrive.

Introduction

Berachain is an EVM Virtual Machine (EVM)-compatible L1 built on top of the Cosmos SDK and derived from the Bong Bears NFT collection in 2021. Proof of Liquidity was born from these memes, which is at the heart of Berachain's mission.

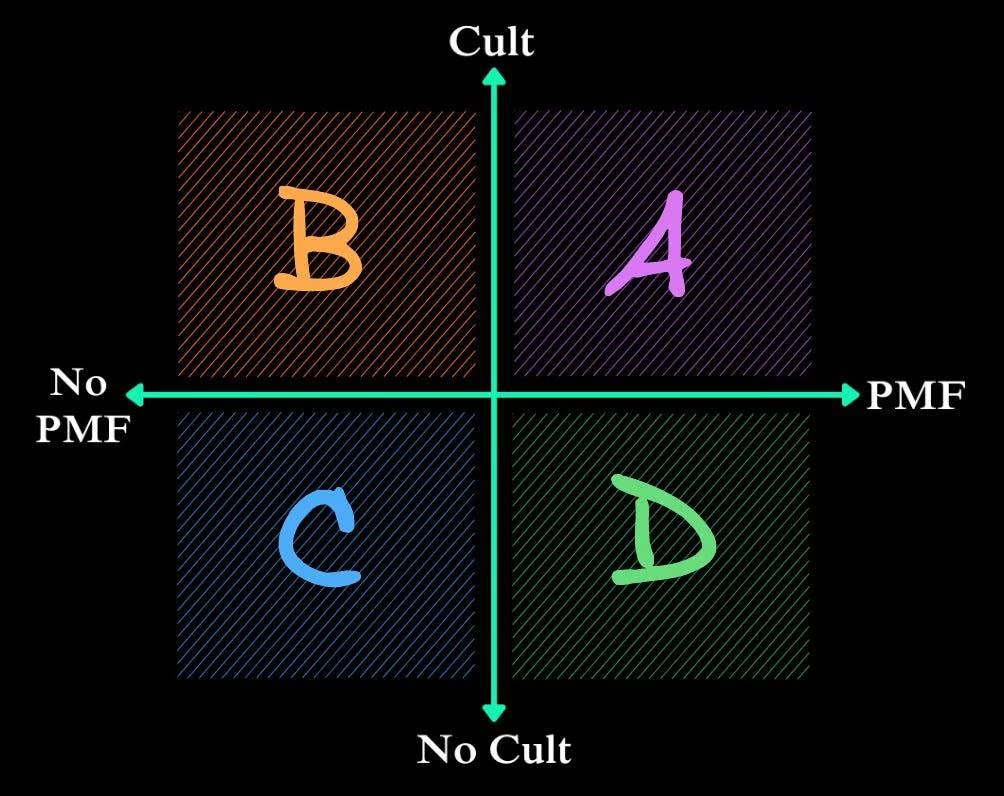

Before you express doubts about Berachain, ask yourself why would you invest in other Tokens? Why do some Tokens maintain ridiculously high fully diluted valuations (FDVs) despite having only a few users? The answer is simple, I think all Tokens are in this range:

- Cult = the amount of time + effort + money invested by the community in an asset

- PMF = Ongoing demand for a given protocol (or speculation on PMF)

- A Quadrant = Send to Valhalla

- Quadrant B = Tokens with a large longest number of high FDV in Crypto Assets today

- Quadrant C = You should probably move to AI

- D Quadrant = Xu long is about to become a middleware/infrastructure Token

Xu long Crypto Assets has billions of dollars in FDV alone with strong community support. In the case of Cardano, the Cardano community somehow continues to rise and gain recognition in the retail market, despite having an FDV of around $18 billion without users and total TVL value. Other examples that focus primarily on assets (in addition to memes) include Litecoin, Cronos, and others.

Is this a bad thing? Just like the protocol of the internet (HTTPS, TCP/IP, etc.), the blockchain itself will eventually become synonymous, which means that the main difference in launching a successful Blockchain is the brand. People trust brands, so Blockchain either becomes a brand or dies.

Bera Community

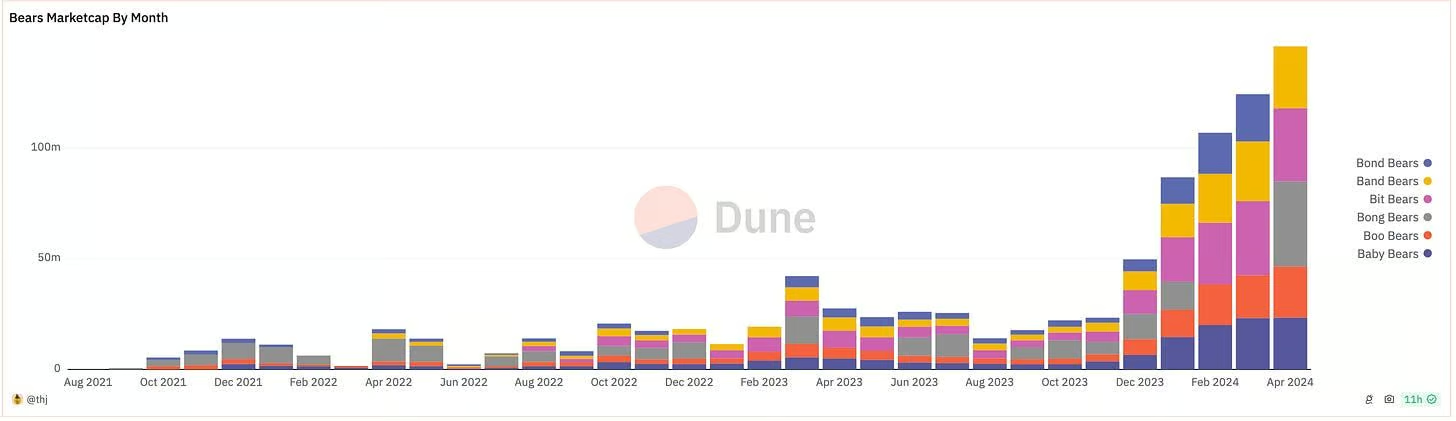

It goes without saying that Berachain has one of the strongest brands in the Crypto Assets space. But long stronger?

The market capitalization of the Bong Bear genesis series and its new version is approximately $150 million or more, and the price, volume, and holdings have continued to rise over the past 2 years.

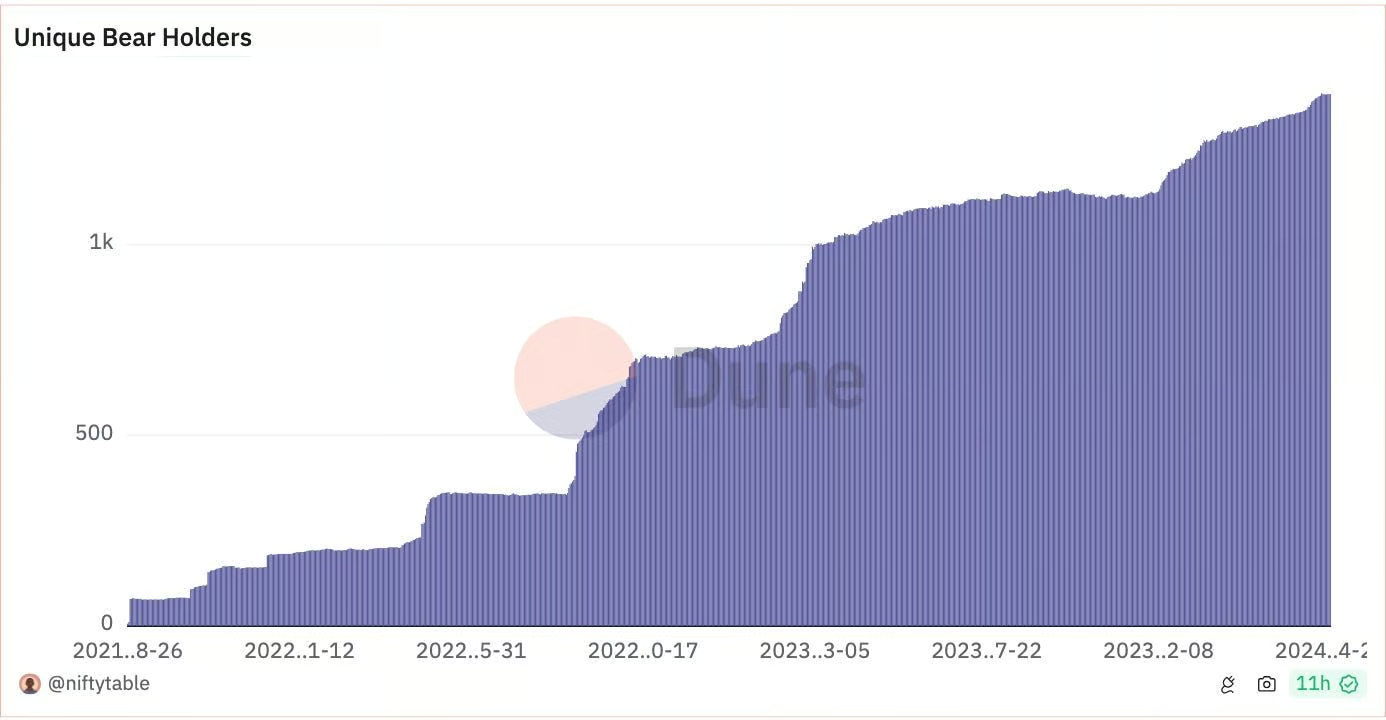

One interesting thing to note is that early holders are rewarded handsomely (e.g. Chainlink, Axie, etc.), and your community thrives on its own, almost forming a life of its own. Take, for example, "The Honey Jar", a Berachain community-run project led by Janitoor. Jani started out as a Large Investors at Bong Bear and now runs a team of over 20 people and has attracted more than 100,000 users to the Berachain ecosystem.

The Honey Jar

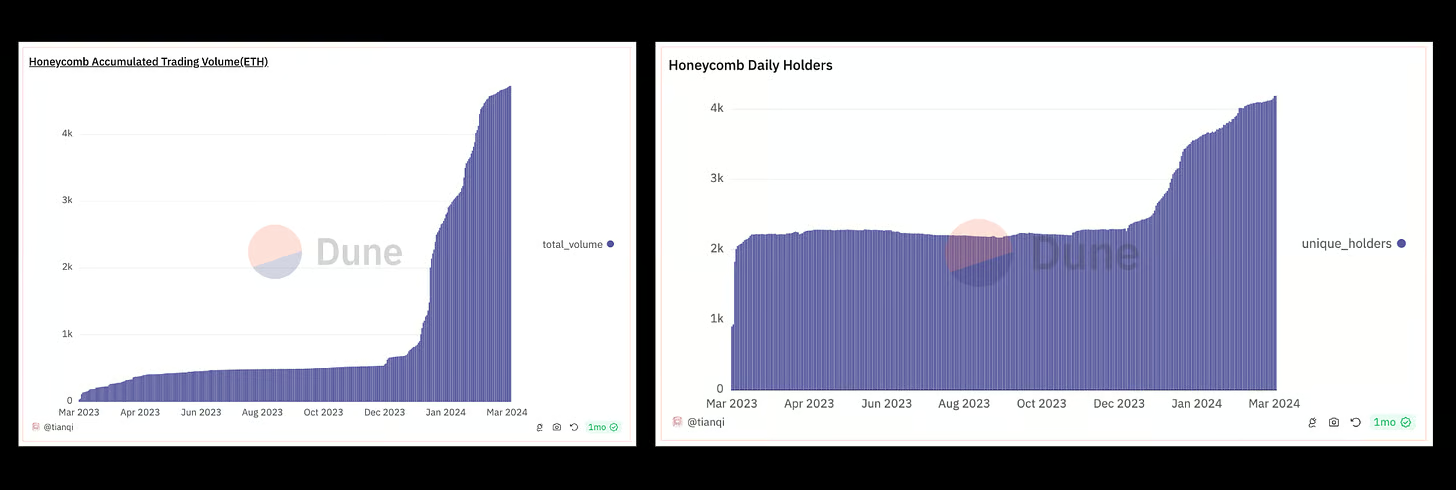

The Honey Jar, or THJ, is the core of the Berachain community and was founded by Jani in January 2023. In Bear Market, THJ has worked as hard as any other project, creating countless lore articles, contests, podcasts, short rooms, NFT minting, and more, gradually building one of the most long prolific communities in the encryption field. At the heart of this community is an NFT collection called "Honeycomb" with a total of 16, 420 NFTs that serve as a "welfare aggregator" for the THJ ecosystem.

An interesting statistic about NFT collections: 4,229 people claimed their NFTs for free, with 1,569 holding them for more than a year despite the price reaching more than 0.6 ETH. In addition to NFT collections, the community has also run long social experiments on Mirror and Zora, where community members can minting THJ lore articles/assets. THJ quickly became the highest-paid author on Mirror, with more than 25% of all Mirror fundraising being THJ assets.

The THJ community also dominates Base and Optimism on Zora

Basically, the THJ's community (and Berachain by extension) has proven a higher "cult" index than any other project: they are willing to spend a lot of time, effort, and money.

But why go through all this trouble before the Mainnet?

According to Janitoor (@deepname 99), "THJ's strategy has always been to create outposts in large communities and protocol and L1s, creating wormholes to Berachain by giving others a chance to experience Beraculture and Berapil and give them a chance to earn some fur in the game ('Berachain is the target chain')"

Jani made this argument a year long ago, and it's crucial to be prepared for the influx of new users and capital, and to provide them with rich content. A year later, this assertion was validated.

What are the implications? All I can say is that there are few, if any, projects that have a superweapon like THJ.

Ecosystem

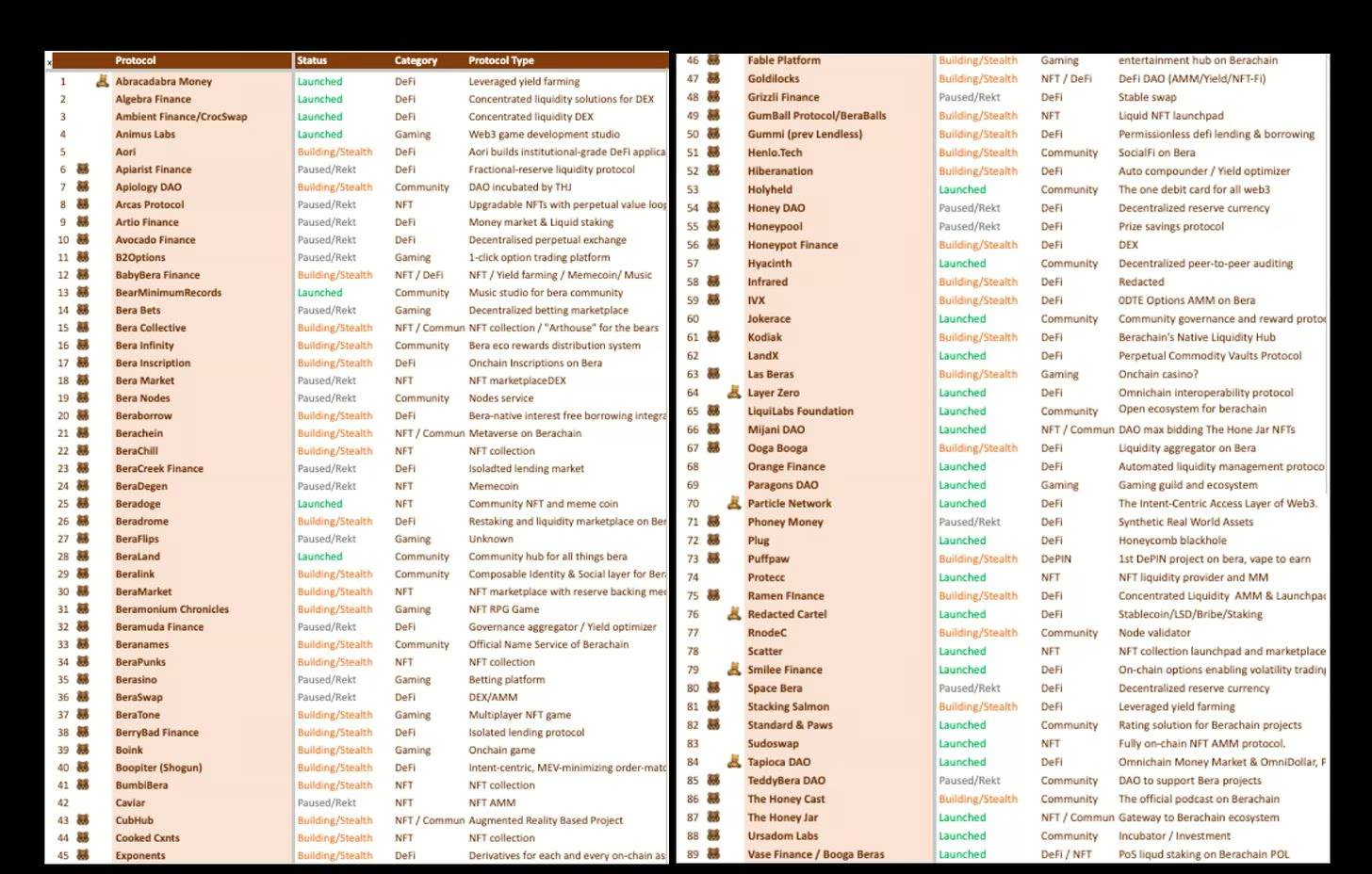

There's a rich community of over 60 Berachain exclusive projects: from re-stake protocol, indie games, coin marketplaces, NFT AMMs, Liquidity aggregators, launchpads, and more. In addition, there are long venture capital-backed Berachain native projects, including Infrared Finance, Kodiak, Beraborrow, Gummi, Beratone, and more.

Other examples of Berachain community efforts include The HoneyCast, a Berachain-native podcast that has been recording shows for about 2 years; Beraland, a community-run Berachain Discord hub/project aggregator, etc.

In addition to the thriving Bera native ecosystem, any existing EVM dApp can be easily ported to Berachain. Some long chain deployments include Ambient, Thetanuts, Concrete...... There are longer yet to be announced.

Of course, it's hard to talk about the Bera ecosystem without mentioning Berapalooza, the hottest event for ETH Denver, which is now a core hotspot for Framework, co-leading the latest funding round.

Well, Berachain has memes, so what?

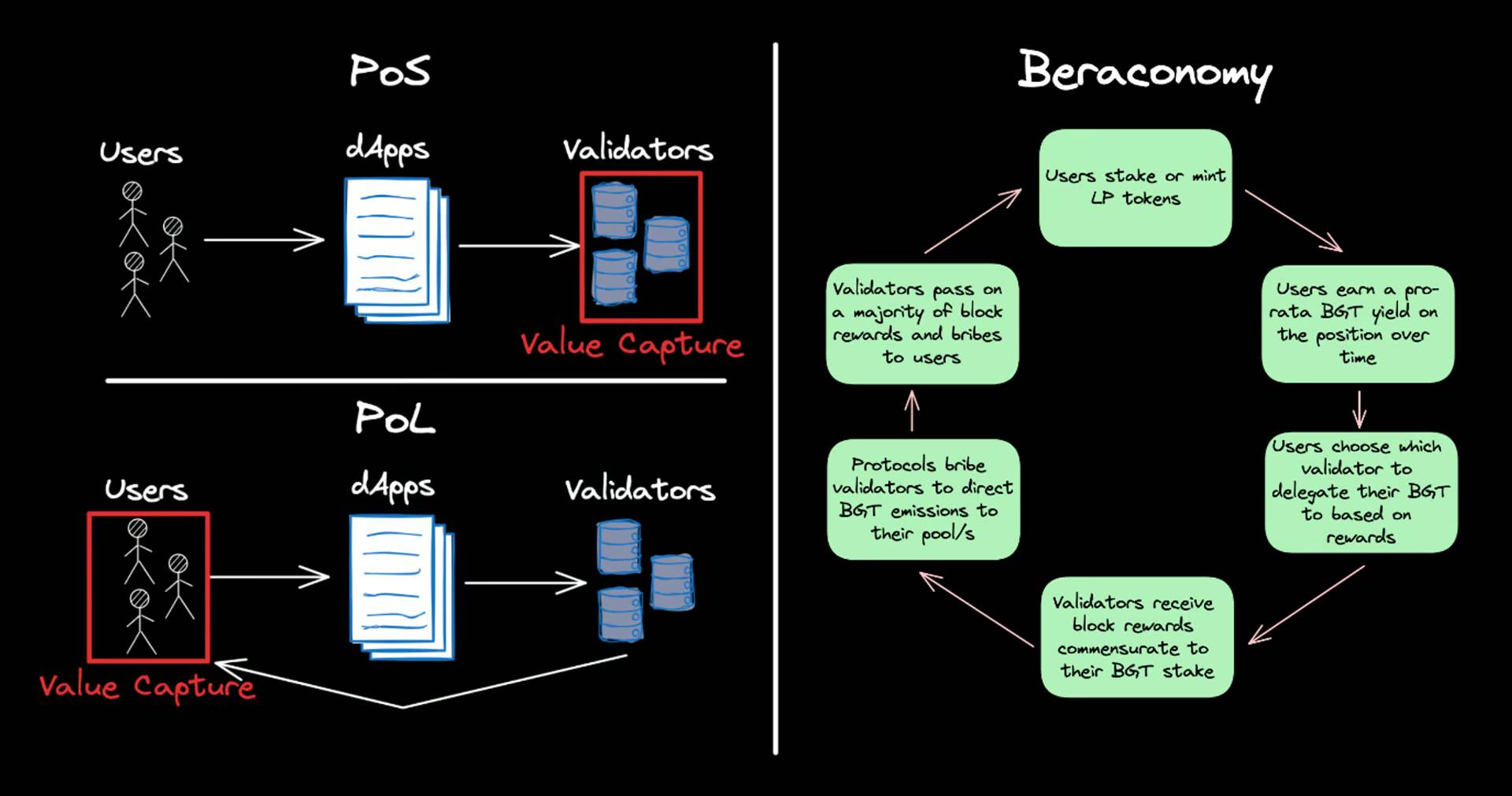

I'm not going to sit here and sell you a breakthrough EVM-compatible CometBFT chain. I think building EVM compatibility and integrating existing technology stacks is key. However, I can say that Proof of Liquidity (PoL) is an intergenerational experiment in Decentralized Finance.

ELI 5 Proof of Liquidity

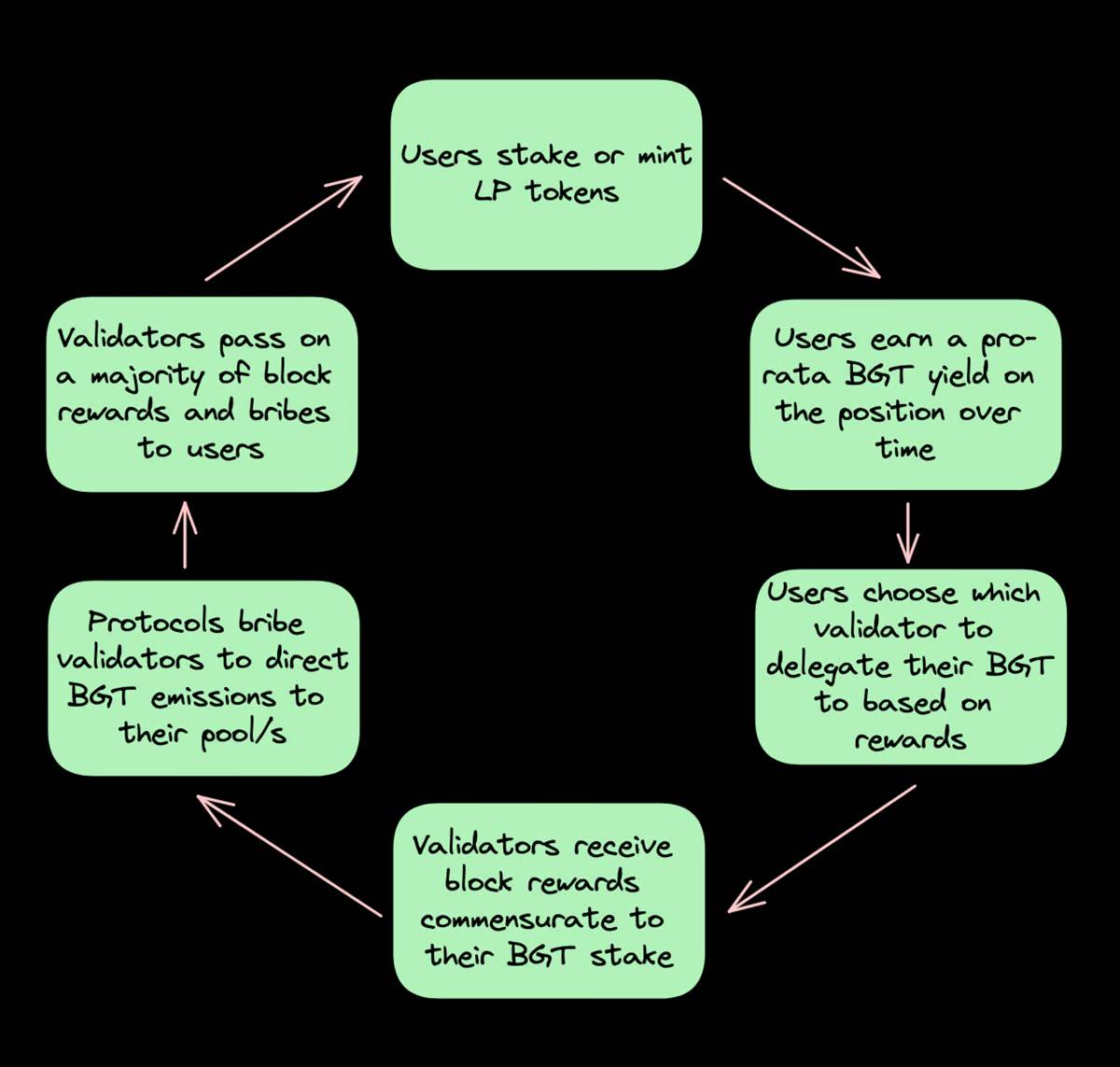

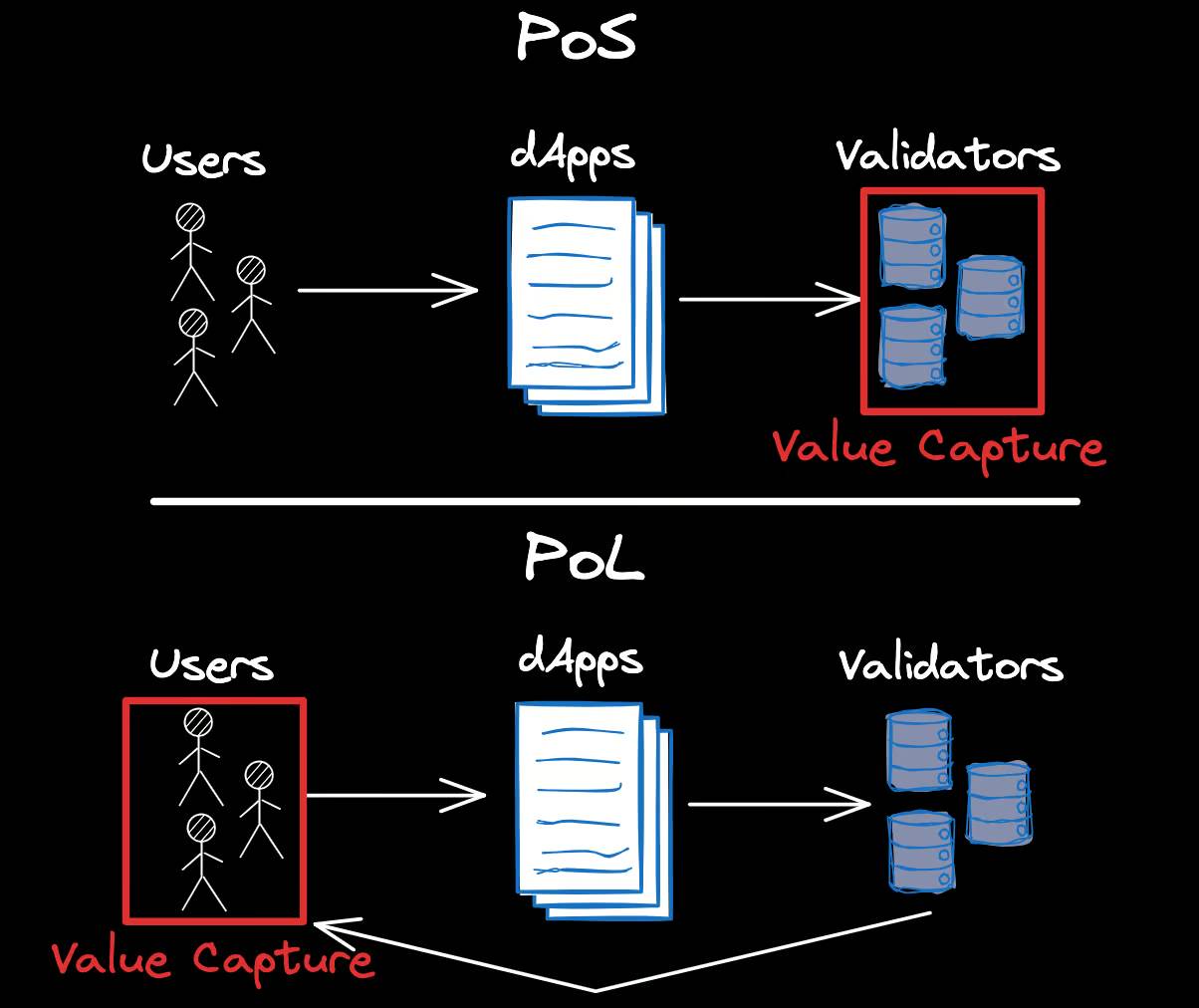

PoL is a novel reward mechanism for aligning users, dApps, and validators. In short, users hold/mint coin LP Token and earn BGT, and these BGT can be delegated to validators validators receive Block Reward commensurate with their BGT shares. Therefore, security is directly linked to liquidity. More specifically, please refer to:

There are still some limitations to attestation of stake (PoS) networks:

- Improving the economic security of the chain reduces ecosystem liquidity

- Concentration of interests in a small number of participants (LSTs/NoOps)

- Lack of coordination between dApps and the underlying protocol

PoL aims to solve PoS-related problems by introducing a dual Token model that separates network Token (BERA) and Governance Token (BGT). With this separation, we can:

- Systematically build liquidity while improving security, which contributes to efficient trading and sustainable network rise

- Align protocol and validators to enable superior coordination of incentives through LP pools, bribery, governance token, etc.

The most exciting part of the PoL is that it enables any dApp to "accelerate" its rise in a utilitarian way, a decision made by the people who initially provided "value" or Liquidity to the ecosystem, i.e., BGT holders (i.e., users).

To clarify, the goals of ETH and Berachain are fundamentally different. ETH aims to be a WW 3 censorship-resistant layer for all value precipitation, while Berachain aims to be a canvas for infinite economic games. In addition, Berachain has declared that it is an ETH neighboring chain.

That's great, but won't the chain be hit hard by Impermanent Loss?

I've heard longest people who know PoL say that Berachain won't be hit hard by Impermanent Loss because its network security relies on staking/minting LP Tokens?

First of all, I would like to say that there is no silver bullet for LP profitability. DEX designs are rapidly improving, and we're seeing the rise of MEV-conscious designs that return value to the application layer, but the question of LP monetization remains fundamentally unresolved.

So will Berachain collapse over time? I don't think so, for the following reasons:

- In addition to providing liquidity to the DEX, there are other ways to earn BGT. Various establishments will be listed in Allowlist (WL) for BGT emissions, whether it is a coin market, Options protocol, etc. Note that any dApp (native or not) can be BGT drained by WL.

- Contrary to the MEV-Boost paradigm, where there is a proposer monopoly on ETH, PoL incentivizes validators (and even protocols) to return most of the profits to users. So, although LPing itself may not be profitable, LPs may receive sufficient rebates through validator bribes or increased block rewards. Therefore, I believe that Berachain is the canvas for the infinite economy game, as the user's money will eventually be returned to the user.

- Finally, there are options to temporarily hedge losses against LPs generated by BGT. Smilee Finance and GammaSwapLabs have already committed to offering such a product on Berachain.

Note that there will also be stable pools that provide a secure source of earnings.

What if most of the liquidity leaves the ecosystem?

BGT does not stop production. Instead, it flows to a smaller, more concentrated group of LPs at extremely high annual intrerest rates. As a result, speculators are likely to keep Berachain in some sort of equilibrium.

In contrast to PoS networks, where network rewards are primarily accumulated by experienced actors, PoL brings value to its users, thereby promoting the long-term health of the Decentralized Finance ecosystem as liquidity draws attention and motivity.

So will Berachain work? Doubts about 0.1 trillion FDV

To be honest, I don't know if Berachain will work. I have a few concerns:

- I think PoL can only work as expected in an efficient market.

- Similar to LRT, I would like to know that in order to get a more long BGT authorization/emissions there will be long less behind-the-scenes dealings.

- There may be a concentration of benefits around a single LST provider.

But here's what I'm going to say. As someone who has been working in the Decentralized Finance space for more than 6 years, Berachain is one of the largest and first Decentralized Finance experiments I've ever seen. While we don't yet know what games will be played, I'm very much looking forward to seeing these Beras push the boundaries of Crypto Assets.

- Reward

- like

- 1

- Share

Moses‘ disciples are the usual tricks of the Jews: the so-called MeMe index is "only for entertainment", "the number of sissies 🈯️", "the number of stars 🈯️", "the number of licking dogs 🈯️" and other rich people‘s entertainment of human nature, which makes people lose themselves and turn into zombies, in the bottomless entertainment, life is fragile, what is their motivation? In the process of enslaving the new humanity!

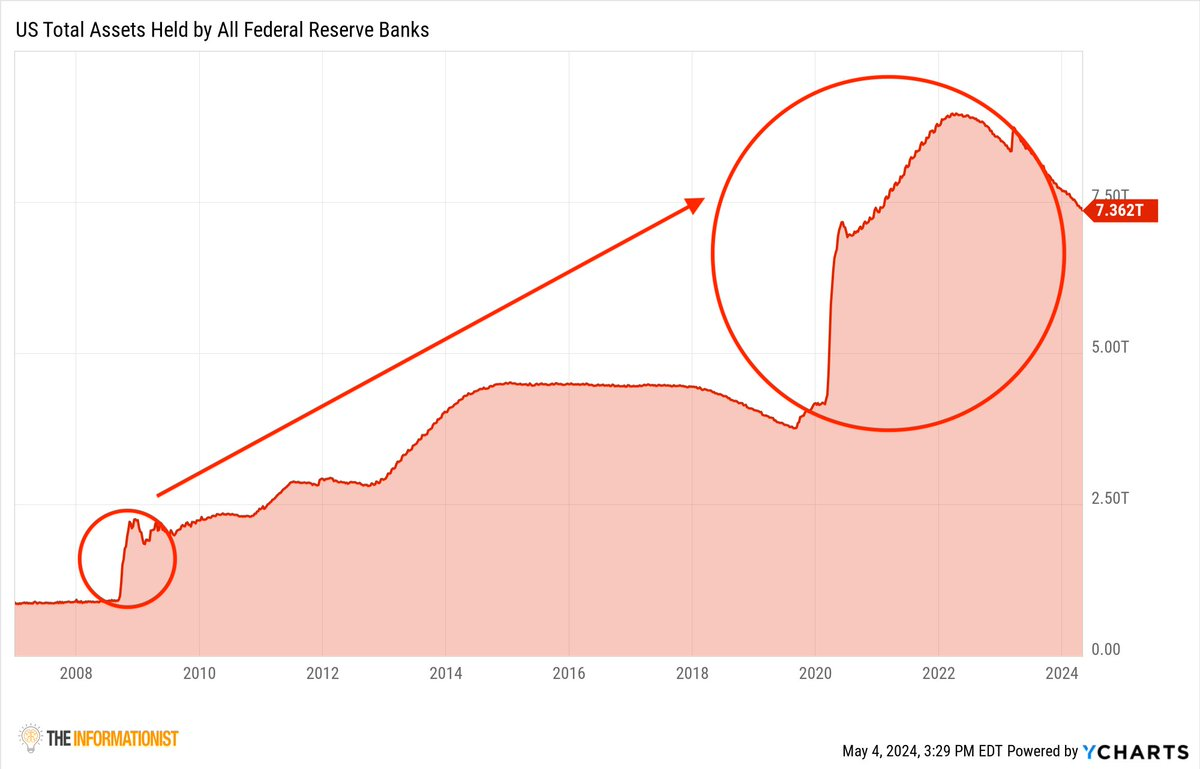

Demystifying the Fed‘s "Money Printing" Routine: The Underlying Reasons Behind Bond Issuance

Original by James Lavish

Original compilation: Deep Tide TechFlow

"Printing money" may seem simple, but it can be confusing. Why sell bonds to the public when the Fed can print longest dollars and pay whatever the government has to spend? The answer is simple, but it requires a bit of critical thinking.

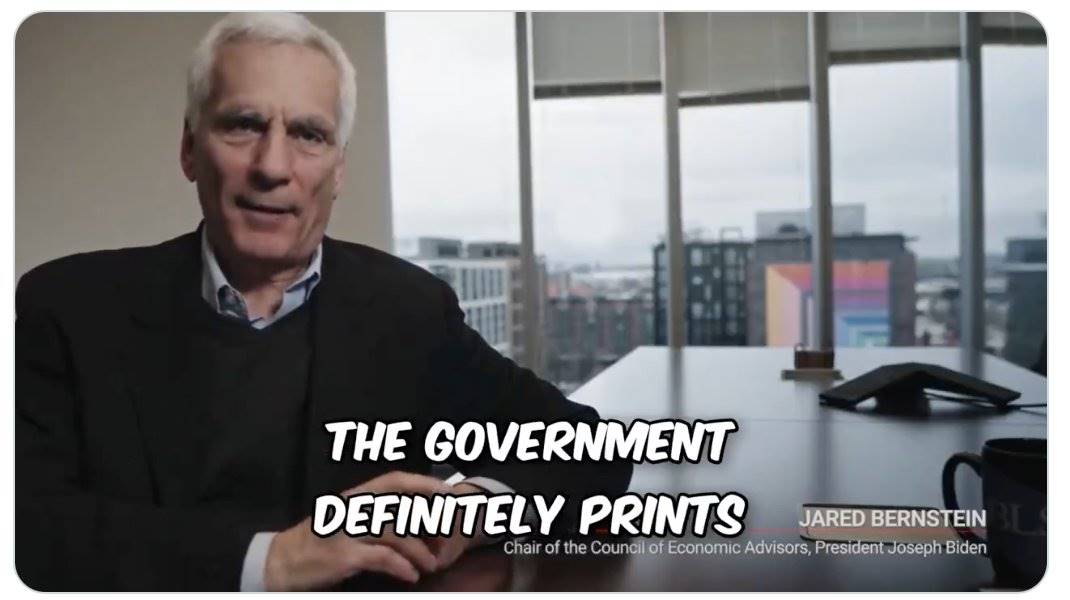

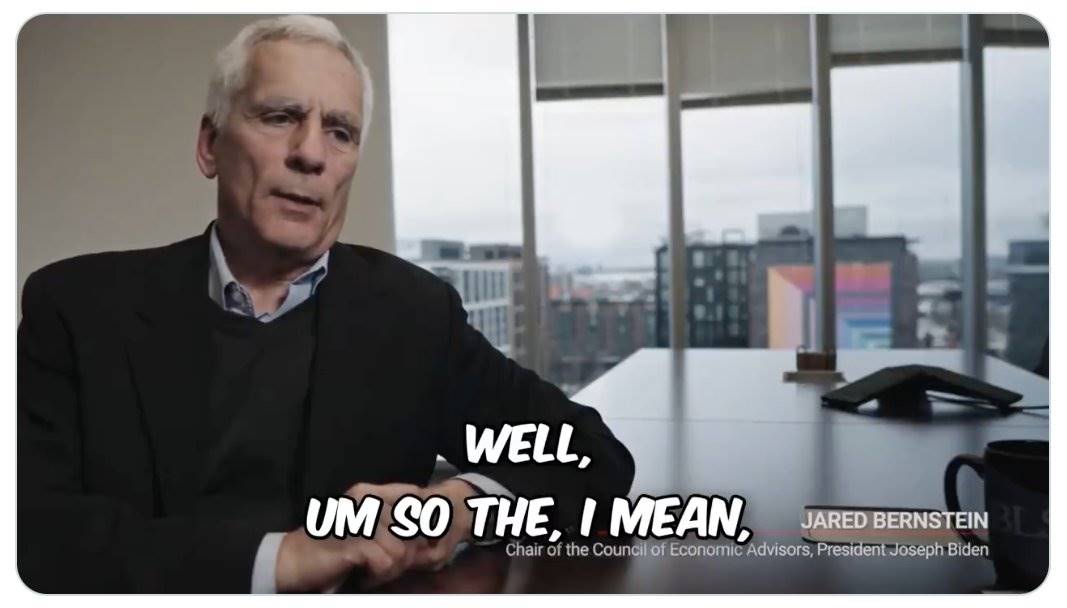

If you've visited Twitter last week, you've probably seen video clips of Jared Bernstein, chairman of the Council of Economic Advisers (an organization that advises the White House on economic policy), "explaining" bonds.

Even so, he seems to have a real hard time understanding the basic concept of national debt and how it works. Honestly, these concepts are really hard to grasp, so let's break them down simply and clearly so that you can understand.

coin supply basics

To understand "money printing", we must first understand the basics of coins. Or rather, the basics of "coin supply", which we will keep at a very high level and make it easy to understand.

Narrow money

Among the Money Supply measures, the strictest is the so-called Narrow Money, which is M 0 ('em-zero'). This only includes coins in circulation and cash in bank reserves. M 0 is often referred to as the base coin. Rising one level, we have the so-called M 1. M 1 includes all M 0 plus demand deposits, plus any outstanding traveler's checks. A demand deposit is simply a liquidity deposit in a bank account that customers can withdraw at any time, i.e. customer checking and savings.

Banks don't keep all their cash in their vaults, they use risk analysis to estimate how little money long available to individual branches in the event that the bank doesn't have bank run, and all that's left is the 0s and 1s on the digital ledger they keep.

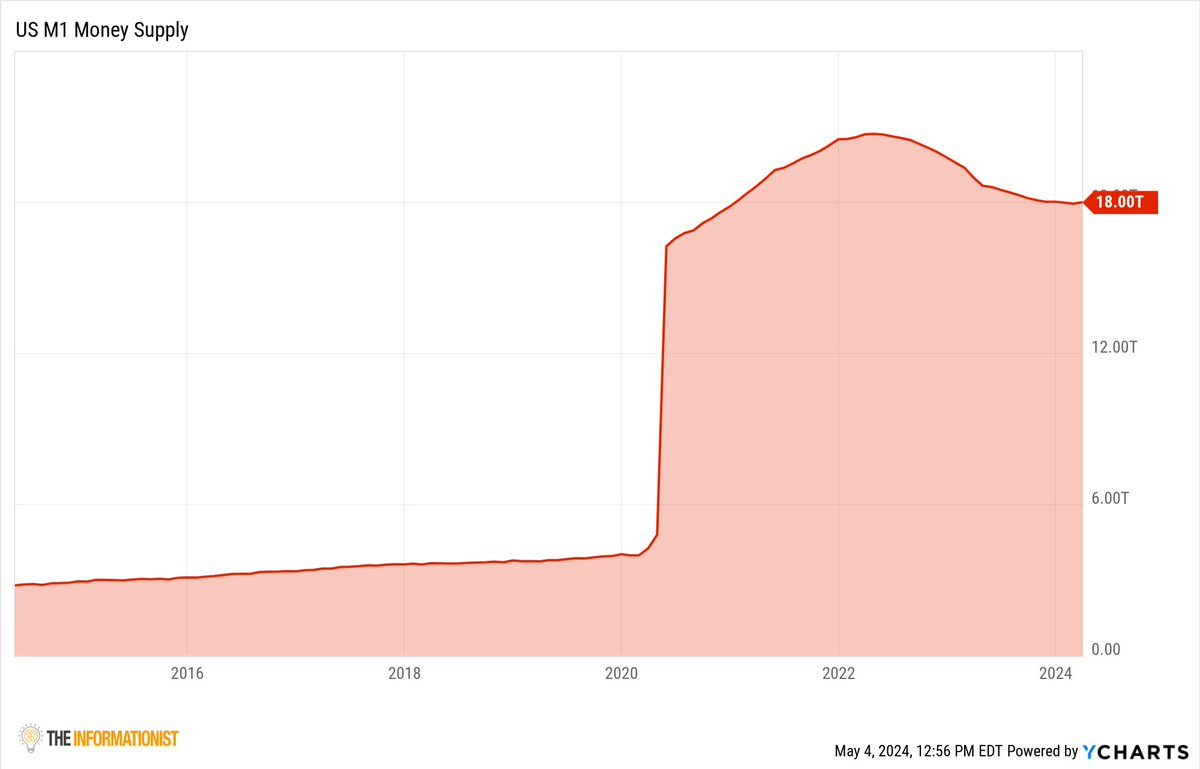

In any case, the M1 includes any cash that can be withdrawn (including those traveler's checks) and that's it. Therefore, M 1 is often referred to as Narrow Money, and here is the dollar amount of M 1:

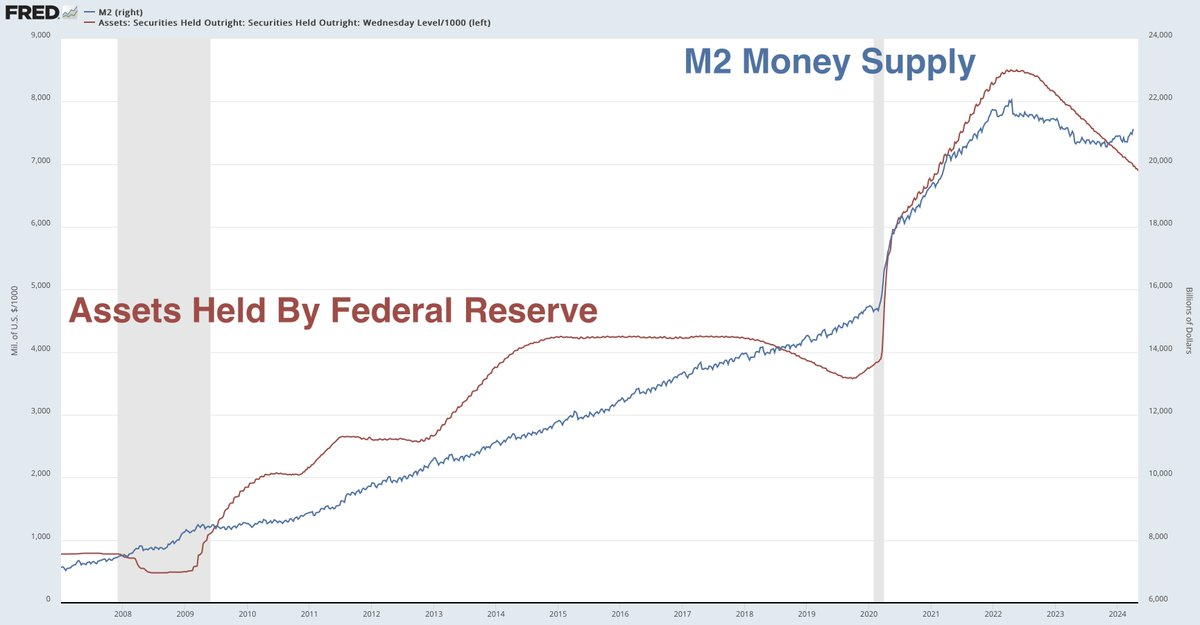

I know what you're thinking: What really happened in 2020 that caused the M1 Money Supply to soar? You guessed it: by printing money. We'll talk about that later, but let's first unpack the next level of coin supply, which is broad money.

Broad money

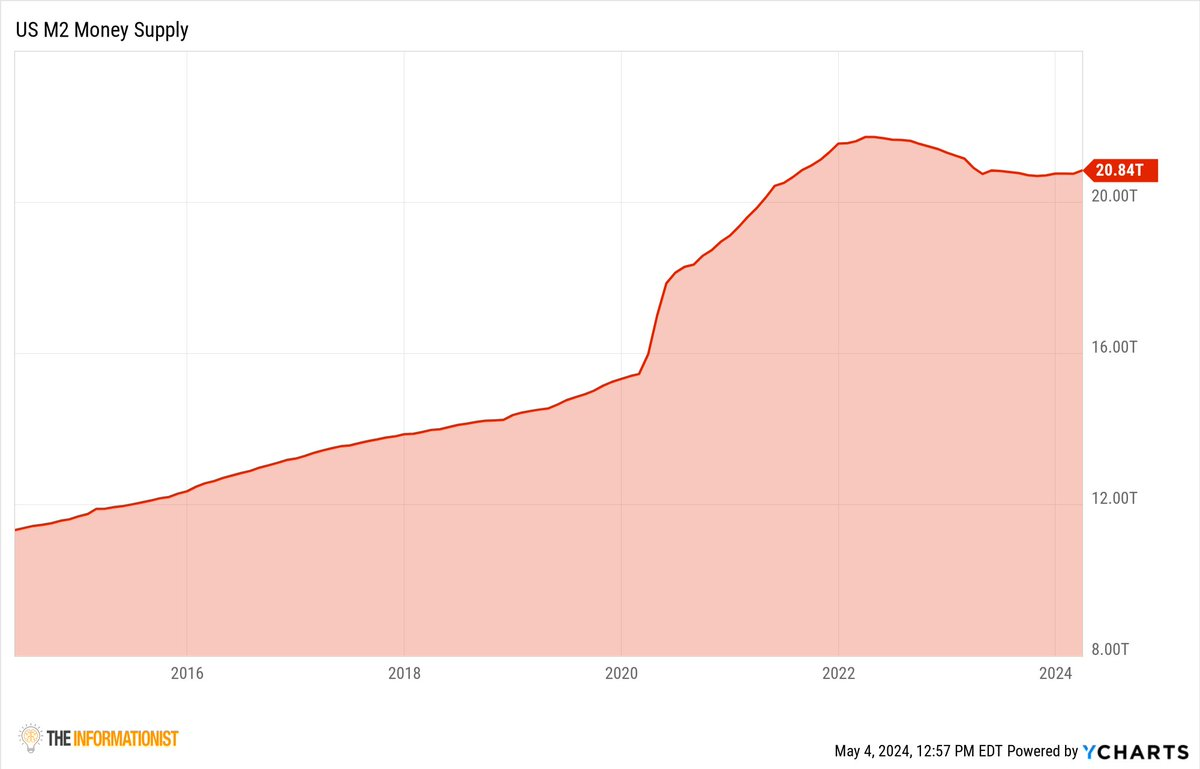

Expanding our scope a bit, M2 includes all M 1 plus coin market savings deposits, time-limited deposits under $100,000 (i.e. CD and coin markets). In other words, M2 includes all funds held in cash equivalents account, Liquidity, and semi-Liquidity account.

Expand to M 2, which is the dollar amount today. You can see how the expansion of the M2 chart after 2020 is gradually expanding and how it takes a while to "penetrate" into personal accounts.

Why? Because of the Cantillon Effect. Named after the 18th-century economist Richard Cantillon, the Cantillon Effect describes how those who receive new money first (i.e., banks, governments, or financial institutions) benefit while others experience a latency effect.

Now, let's explain the difficulties that Jared Bernstein had in describing (apparently he himself did not understand) US Treasuries.

Treasury Basics

In its most basic definition, U.S. Treasuries are bonds issued by the U.S. government. This is no different from the bonds of Apple, Microsoft or TSL issuance, except that this is the state (or company) borrowing money from the person who buys the bond.

What happens when you borrow money? You pay Interest to the person who lent you money, just like the bank Interest you pay your mortgage. You borrow money from the bank to buy a house, and you pay bank interests on that loan. We all know that the government has been borrowing heavily lately, and this is because the government is in deficit (spending more than tax revenues) and borrowing to make up the difference, which has increased the U.S. public debt.

The United States borrowed longest or less, and owed longest or less money to everyone who lent it money?

Can you believe it, that's a total of $34.6 trillion!

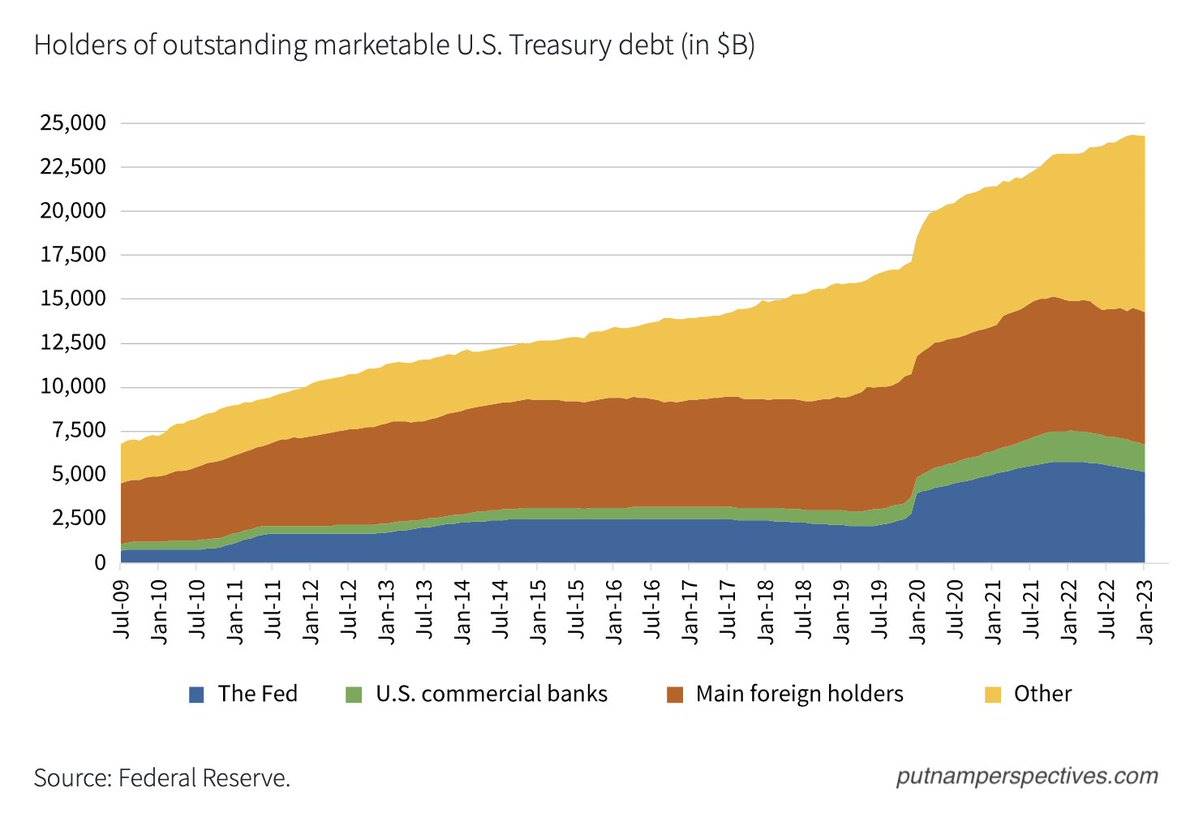

So who's buying all these bonds? That is, who lent the United States such long money?

Basically, you and I, as well as others, buy bonds directly in their IRAs, 401 Ks, personal accounts, and indirectly through mutual funds and coin markets, Bank of America, foreign central banks (i.e., Bank of Japan, Bank of China, and other foreign countries), including the Fed itself buying bonds.

You may be asking, how is it possible that they have all these US Treasury bonds? Let me explain step by step.

How money is "printed".

This involves quantitative easing (QE) and quantitative tightening (QT).

In times of financial crisis or recession, such as the financial crisis, we see the Fed using QE in a shotgun fashion, recklessly buying US Treasuries and MBS (mortgage-backed securities) QT is the time when the Fed sells them back to the market.

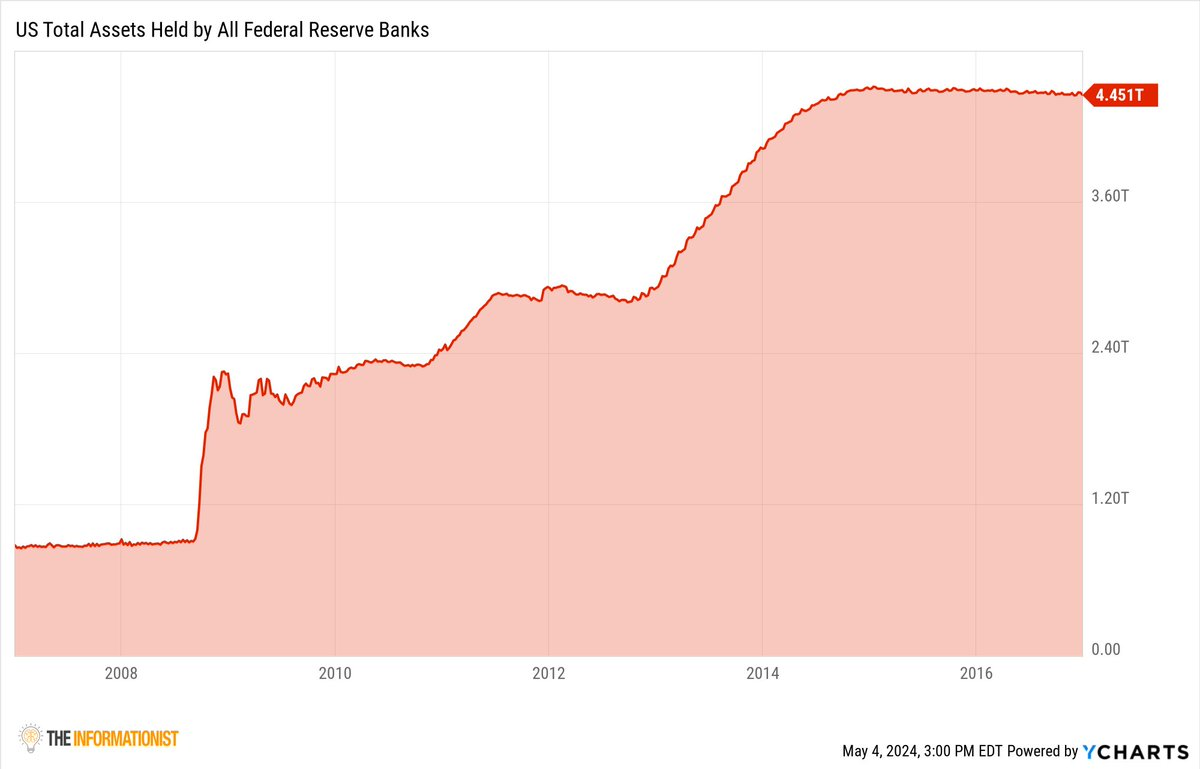

During the global financial crisis QE, the Fed bought more than $1.5 trillion of these assets over a few years (and then continued to add for several years).

Fast forward to 2020, markets are struggling due to pandemic lockdowns, and the Fed has added cash "bazookas" to its cannon. This represents an increase of more than $5 trillion in just 2 years, look at the difference between 2009 and 2020.

But how do they do it?

As the central bank of the United States, the Federal Reserve has a unique ability to create coins. When the Fed uses QE to buy securities such as Treasuries, it does so by creating bank reserves out of shorts, which is the digitization process of coin creation. Here's how it works:

- The Federal Reserve announced its intention to purchase securities and the amount of their purchases.

- Primary dealers (large intermediary banks) buy these securities in the open market on behalf of the Federal Reserve.

- After the purchase is completed, the Fed credits the newly created coins to the reserve accounts of primary dealers and adds Treasuries to its own balance sheet.

- This process increases the total reserves of these banks, injecting liquidity directly into the banking system.

Essentially, the primary dealer acts as a broker and Settlement the trade, sending those newfound funds to Treasury sellers and Treasuries to the Federal Reserve, and then more long cash goes into the system.

Imagine you're playing a monopoly game, all the money has been allocated and is already in the game, and then, a new player appears in the game with money from "his" house playing Monopoly and he just starts buying property around. Now the situation is that he added new coins to the game that he didn't have before, he expanded the Money Supply, and as a result, Park Place and Boardwalk became more expensive. This is exactly how the Fed operates when it implements QE policy and bond purchases in the open market.

The Fed has injected liquidity into the market by adding coins that were not previously available in the market. See how the M2 Money Supply (blue line) has risen as the Fed's balance sheet expands. This is the typical money printing machine.

As for why we don't skip the whole QE and treasury lending system and print money directly, if we do, we will completely become a so-called "banana republic", blatantly and excessively printing money to finance government deficits leads to vicious Inflation. Imagine a world where the Treasury Department (and indeed Congress) spends as little as it wants, long long as little as it wants, and the Fed prints long as little money as it needs to spend.

Uncontrolled, unabated, undisguised.

With the sharp inflation of Money Supply, prices will pump exponentially (Park Place and Boardwalk will be sold for millions, billions, trillions) and people will lose faith in the dollar as a means of store of value and, at some point, in the dollar as a means of exchange. The streets will be full of dollars, because it takes a cart of dollars to buy anything, and the price changes every minute.

(If you think that's an exaggeration, check out Venezuela or Lebanon for yourself.)

This will lead to a loss of confidence, confusion and a rapid move towards a vicious Inflation, and the dollar will collapse. The Fed and the Treasury will do everything they can to confuse and divert attention from the Infinity Money Printing Machine.

They will sell bonds.

Even if it's sold to themselves.

If the country's chief economists are all confused by the system, others must be confused as well.

Well, the show will continue.

- Reward

- like

- 4

- Share

A quick look at Alliance‘s latest 12 encryption startups

Original author: Deep Tide TechFlow

At this Node when the market is volatile and the market is slightly tired, Alliance is heading out to market with the latest batch of incubated projects.

As the world's largest accelerator in encryption, Alliance has incubated projects such as Tensor, Pendle, Synthetix, etc., and the recently popular encryption consumer apps Fantasy.top and Pump.fun were both incubated by Alliance, and Fantasy.top and Pump.fun are now among the top 10 Crypto Assets protocol in terms of fees and revenue generated, surpassing the established L1s.

Last week, 12 start-up encryption companies successfully "graduated" from Alliance, among which the current popular RWA, AI, and DePIN track projects accounted for longer, and the selection of incubation members reflects Alliance's close understanding of market hotspots and industry narratives.

In addition to controlling the current hot narrative, several projects in this issue focus on exploring the encryption market in Asia, Africa and Latin America, reflecting the current trend of encryption expansion to third world countries.

Here's an introduction to these 12 startups:

1. Villcaso

Product direction: US real estate tokenization

Project Twitter:

Brief introduction:

Villcaso has on-chain tokenization U.S. real estate in a Compliance way, and now users around the world can participate in U.S. real estate investment by holding Villcaso's on-chain Token $USH (U.S. housing), solving the problems of policy Compliance and high barriers to entry faced by non-U.S. residents investing in U.S. real estate.

2.GoBankless

Product direction: cross-border payment of Crypto Assets in Africa

Project Twitter:

Brief introduction:

GoBankless builds a Compliance Stablecoin Cross-border Payment System for African SMEs, a project that helps SMEs convert cash into stablecoins. Through on-chain cross-border payment, it helps African SMEs avoid SWIFT fees of up to 20% and long settlement times, solving the huge pain points of African SMEs. Currently, GoBankless has served longest 400 courier companies and 49 bank branches in Africa.

3. Wasabi Protocol

Product direction: NFT and MEMECOIN derivatives trading

Project Twitter: _protocol

Brief introduction:

Wasabi Protocol is a Web3 long-tail asset derivatives trading built on Blast Chain, providing users with Margin Trading of high-Fluctuation assets (such as NFT, MEMECOIN), as well as services such as NFT Options, asset stake, and fractional NFT trading. It is also the first project to provide derivatives trading for the protocol of ERC 721s and ERC 404 assets, while actively promoting Liquidity problem solving for culturally attributed memecoins. Within months of its launch, Wasabi attracted more than 30,000 users and generated more than $200 million in platform volume.

4.Lulubit

Product direction: Provide fiat currency exchange for Central America

Project Twitter:

Brief introduction:

In order to solve the pain point of the $70 billion Central American Crypto Assets market, which is still dominated by P2P networks with high transaction fees and poor user experience, Lulubit provides Central American users with a fiat exchange Crypto Assets service, which allows users to buy or sell Crypto Assets directly using bank account and use debit cards to spend Crypto Assets. In less than a year, Lulubit has attracted more than 18, 000 users. The product currently serves residents of Panama and Guatemala and will soon be expanded to the rest of Central America.

5.ZwapX

Product direction: tokenization of watch transactions

Project Twitter:

Brief introduction:

Traditional luxury watch trading platforms such as Chrono 24 and Montro have led to an endless stream of fraud incidents around luxury watch transactions due to their imperfect technology for distinguishing the authenticity of watches, and in order to combat fraud, traditional platforms must rely on a deposit custody system to solve this problem.

ZwapX solves this problem by hosting watches for customers instead of funds, users can send the watch to ZwapX's warehouse in Geneva after registering the watch information, and there will be professionals to check the authenticity and condition of the watch before the watch is put into storage, and after confirming the storage, ZwapX will exchange the watch for the corresponding on-chain Token, and the user can choose to hold or freely trade the watch Token. Transaction success funds are delivered immediately to the seller, and the buyer can exchange the token for a physical watch or use it as collateral in Decentralized Finance at any time.

6.Fractal Payments

Product direction: stablecoin cross-border payment

Project Twitter:

Brief introduction:

Fractal Payments is a global cross-border payment platform that supports stablecoin Settlement and Money Laundering is 3x cheaper and Settlement 6x faster than Swift. Traditional cross-border payment solutions face high fees, slow processing times, and complex barriers to use.

Fractal Payments is fully licensed in the European Union and currently supports payments in longest 60 countries. This allows businesses to use on-chain stablecoin for fast and low-cost Settlement while pricing transactions with fiat.

At present, Fractal Payments has been widely used in applications such as Zerion.

7.Codigo

Product direction: artificial intelligence code generation platform

Project Twitter:

Brief introduction:

The usability of an AI model largely depends on the quality of the data on which the model is trained. However, obtaining training data is difficult because the relevant domains are often not well classified, and the quality of the models is uneven. Today, Codigo is committed to making it easy for users to access high-quality training data. The Codigo platform uses tokens as incentives to provide customers with high-quality datasets through data crowdsourcing and centralized review, while providing segmented professional model training services for high-risk AI financial zones. It's worth mentioning that Codigo's initial focus is on encryption Source Code, which is rich in data volume and of excellent quality. Their beta tool generated over 4 million lines of code in just 6 months.

8.Accrue

Product direction: cross-border payment in underdeveloped areas of Africa

Project Twitter:

Brief introduction:

Accrue provides a service for users in the African region to create virtual payment cards, and on the Accrue platform, African users can stablecoin deposit virtual cards in US dollars and Settlement transactions with US dollar stablecoin through long channels, including banks. This approach drops cross-border settlement costs in Africa by nearly 10 times, reducing settlement speed from 2 weeks to 5 minutes. Accrue is currently available in 7 countries and is integrated with Opera, Africa's largest payment wallet app. Since its launch, Accrue has processed more than $5 million in metatransactions.

9.Fig

Product direction: CeFi Options tokenization

Project Twitter:

Brief introduction:

Fig focuses on the CeFi Options market, which is long larger than the CeFi Perptual Futures market, and uses complex Options tokenization to help users easily use Options to on-chain portfolios and use complex Hedging strategies to obtain returns

In the four months since the project was launched, Fig's Options volume has exceeded $50 million, and the ecological TVL has exceeded $10.2 million.

10.0 G

Product direction: artificial intelligence on-chain data availability solutions

Project Twitter: _labs

Brief introduction:

0 Glbs is the first modular AI chain that is building a Programmability data availability solution designed to solve the massive data storage and throughput required for on-chain AI operations, dividing data into two phases: publishing and storage. Officially, this architecture performs 50, 000 times faster than leading data availability solutions such as Celestia, while at 100 times lower cost.

11.Proto

Product direction: Build on-chain Google Maps with DePIN devices

Project Twitter: _proto

Brief introduction:

Proto's DePIN network uses Token incentives to provide up-to-date mapping services for emerging economic industry regions through geographic data uploaded by users' mobile phones. Uploading geographic data through users' mobile phones can solve the problem that large map operators such as Google do not update their information in a timely manner due to the dense construction of urban centers and the rapid change of geographic information in developing countries such as Mumbai and Bangalore.

Within months of going live, Proto had achieved 75% Google Maps coverage in Bangalore, while also providing new coverage in areas where Google Maps couldn't.

12.Dinari

Product direction: tokenization of U.S. stock securities

Project Twitter:

Brief introduction:

Dinari is a Web3-oriented securities asset trading platform, Dinari uses smart contracts to tokenize securities called dShares, allowing users to trade traditional securities assets such as stocks, bonds, and ETFs on the on-chain. Currently, Dinari only runs on Arbitrum and supports the use of stablecoins such as USDC, USDC.e, and USDT to pay for transaction gas, without the need for native tokens such as ETH.

- Reward

- like

- 1

- Share

Bankless Founder: Will Ethereum miss this Bull Market, and which side are you on?

Original author | Ryan Sean Adams

Compile | Golem

Ryan Sean Adams, founder of Bankless, an encryption information and research platform, initiated a discussion on platform X about whether Ethereum will miss this bull market, saying that he will first think about the matter from the perspective of Ethereum long-termists, rather than those who mistakenly believe that Ethereum is dead.

He stated the reasons for missing and not missing both views, and finally asked which side would everyone be on? The following Odaily Planet has compiled the two views below, and readers should vote too.

Ethereum will miss this Bull Market: New users are not choosing Ethereum

Ethereum is in adolescence and is going through an awkward phase of mood Fluctuation like a teenager, trying to move towards adulthood but the world doesn't understand him.

The biggest factor is L2. This cycle of Ethereum is different from the past because it's basically telling new users, "Hey, don't use Ethereum, we're too expensive, but the good news is that we have 100 brand new L2s and you're going to love them." So countless L2s built cross-chain bridges, then dispersed liquidity, and finally ended in failure and so on.

But in the long run, developing Ethereum L2 is the right thing to do, the best long-term way to achieve Decentralization, and Vitalik's vision and so on. These things don't have to be told over and over again to someone who has been believing in this since 2021. But the problem is that they are not new buyers of ETH.

So who should the new buyer be? It's those who speculate on meme coins, app users, and people from TradFi.

But the first two are busy buying tokens on the on-chain they are using, while L2 beat shows 96 chains to choose from. Lastly, people from TradFi are buying Bitcoin and they won't care if on-chain have long less real cash flow.

While the issue of fragmented liquidity is being addressed, fundamentals are also important. But now is the adolescent of Ethereum, and when some chains are taking shortcuts, Ethereum has to grit its teeth and take the difficult road and go through the necessary awkward phases in order to become a mature and well-functioning chain.

It's a long-term thing, but it won't pay off in this cycle.

ETH Bull Market is coming: the fundamentals are good and Ethereum dominant

Others will disagree with the first argument and argue that the ETH will reach $10,000 when the BTC Bull Market comes.

The current Ethereum is too strong long compared to the 2020 stage. Not only is it a profitable Blockchain, but it also has a solid tokenomics, with the world's largest exchange doing Ethereum L2, ZkEVMs already happening, unlimited L2 budgets are accelerating the development of Ethereum technologies, Ethereum ETF is also coming soon, BlackRock's tokenization Treasuries, and more. Ethereum's fundamentals are positive.

Some chains may have 1 million users, but Ethereum can be the underlying infrastructure of 1000 chains, and the fees of 1 million users on each on-chain will be returned to Ethereum. L2 decentralized liquidity will also be fused because L2 chains are accumulating huge centralized debt, which they will later pay back to Ethereum and pay Ethereum through gas.

For investors who are eyeing BTC's new narrative, it's only a matter of time before they wake up and start valuing cash flow.